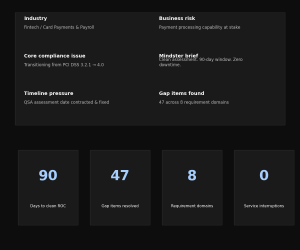

PCI DSS 4.0 has changed how fintech companies approach payment security, compliance governance, and audit readiness. This blog explains how Mindster helped a fintech payroll platform achieve PCI DSS 4.0 compliance readiness in 90 days by restructuring security controls, remediating infrastructure gaps, aligning engineering workflows with compliance requirements, and preparing the organization for QSA assessment without disrupting live payment operations.

The article breaks down the complete implementation journey — from the initial gap assessment and architecture review to technical remediation, evidence collection, and audit preparation. It also explains the operational decisions, security priorities, and execution principles that enabled the fintech platform to meet PCI DSS 4.0 requirements within a fixed timeline while maintaining business continuity.

When the client approached Mindster, the organization was operating with an existing PCI DSS 3.2.1 compliance posture and an approaching QSA assessment deadline. However, several critical gaps had already emerged:

* Administrative access systems were not fully aligned with PCI DSS 4.0 MFA requirements

* Security monitoring relied heavily on manual review workflows

* Vulnerability management processes were periodic rather than continuous

* Policy documentation no longer accurately reflected live production controls

At the same time, the platform could not afford disruption to active payment processing and salary disbursement operations during remediation.

The challenge was not simply achieving compliance. The challenge was restructuring security operations, engineering workflows, and governance controls within a 90-day assessment window while maintaining business continuity.

Why PCI DSS 4.0 Is a Different Problem Than Version 3.2.1

For fintech companies processing card payments at scale, PCI DSS 4.0 introduces three operational challenges that a traditional compliance checklist cannot solve:

1. Authentication Becomes an Infrastructure Requirement

Multi-factor authentication is now mandatory across all non-console administrative access and all remote access into the cardholder data environment. This impacts infrastructure architecture, privileged access workflows, and DevOps operations.

2. Continuous Validation Replaces Periodic Audits

Security controls must now be continuously monitored and validated. Quarterly manual reviews are no longer sufficient for critical systems and configurations.

3. Compliance Decisions Must Be Defensible

Organizations using customized implementations must document why controls were implemented a certain way, how risk was evaluated, and how effectiveness is continuously measured.

For fintech companies whose payment processing capability depends on PCI DSS certification, version 4.0 changes the problem from periodic audit preparation to continuous operational security. The challenge is no longer implementing controls once — it is proving that those controls are continuously validated, monitored, and governed across infrastructure, engineering workflows, and production operations.

The Client: A Growing Fintech Brand Processing at Scale

Our client operates a card payment and salary disbursement platform serving enterprise employers and their workforces. The platform handles salary processing, card management, and remittance services for a large user base across a regulated financial market.

A QSA (Qualified Security Assessor) assessment was approaching. The existing compliance posture had been built against PCI DSS 3.2.1 — which meant that the MFA architecture, monitoring logic, and documentation framework were structurally misaligned with version 4.0 requirements.

The business stakes were direct: the payment processing capability underpinning the entire product could not operate without a valid PCI DSS assessment. There was no option to delay.

The brief Mindster received:

- Achieve a clean PCI DSS 4.0 QSA assessment

- 90-day window from kick-off to assessment-ready

- No disruption to live payment processing during remediation

- Build controls that would hold beyond the assessment cycle

What the gap assessment revealed

Before any remediation begins, the first priority is always a structured gap assessment. For this client, four primary problem areas surfaced — each requiring different types of remediation work.

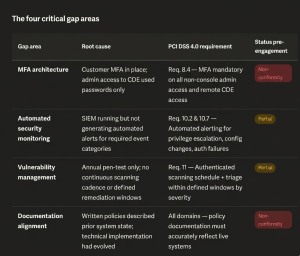

1. Multi-Factor Authentication Was Incomplete

The client had MFA deployed on customer-facing access. Administrative access to the cardholder data environment — including system consoles, database access, and infrastructure management — relied on password-based authentication. Under PCI DSS 4.0 Requirement 8.4, this is a direct non-conformity. There are no exceptions.

2. Automated Monitoring Had Gaps

Intrusion detection was running, but security event monitoring was not generating automated alerts for several categories of events that 4.0 requires — including failed authentication patterns, privilege escalation, and configuration changes on critical systems. The Security Operations team was reviewing logs manually on a scheduled basis.

3. Vulnerability Management Was Reactive, Not Continuous

Internal and external penetration tests were conducted annually. PCI DSS 4.0 Requirement 11 now requires authenticated scanning and a structured process for responding to newly discovered vulnerabilities within defined windows, independent of scheduled test cycles.

4. Policy Documentation Did Not Reflect Actual Controls

This is the most common gap we find. The written security policies described controls that had evolved since they were written. In several cases, the policy described a process that no longer matched the actual technical implementation. Under version 4.0, this misalignment fails the assessment regardless of whether the technical control itself is sound.

The four critical gap areas

The 90-day remediation roadmap

Ninety days is sufficient to achieve PCI DSS 4.0 compliance for a fintech organization with an existing compliance foundation — but it requires structured planning and a hard rule: no remediation begins until the gap picture is complete and signed off. Implementation that starts without a complete gap picture creates rework.

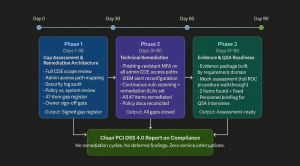

Phase 1 (Days 1–30): Gap Assessment and Remediation Architecture

The first month is structured discovery and planning, not implementation. Implementation that begins without a complete gap picture creates rework.

What happened:

- Full technical review of the cardholder data environment scope

- Mapping of all administrative access paths and authentication methods

- Security event log review to identify monitoring gaps

- Documentation audit: written policies matched against actual system configurations

- Prioritized gap register with technical remediation specifications for each item

At the end of Phase 1, the client’s engineering, security, and compliance leadership signed off on a remediation plan with defined owners for every gap item. Nothing proceeded to implementation without that sign-off.

The output: A structured gap register with 47 items across eight PCI DSS 4.0 requirement domains, each mapped to a remediation owner, technical specification, and target completion date.

Phase 2 (Days 31–60): Technical Remediation

This is where the engineering work happens. We operate a dedicated fintech engineering team that understands the intersection of security architecture and payment system operations. Changes to the cardholder data environment cannot be tested in isolation from the payment processing workflows they protect.

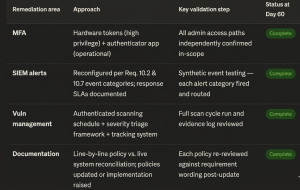

MFA Implementation

We deployed phishing-resistant MFA across all administrative access paths to the cardholder data environment. This included system console access, database administration tools, infrastructure management interfaces, and CI/CD pipeline access that could modify production environments. The implementation used a hardware token approach for the highest-privilege access roles, combined with authenticator-based MFA for operational access.

This work required coordination with the client’s infrastructure team and their cloud provider, and was staged to avoid service interruption.

Automated Security Monitoring

We implemented a SIEM configuration that generated automated alerts for the event categories required by PCI DSS 4.0, including privilege escalation events, configuration changes on in-scope systems, and authentication failure patterns. Alert routing was tested against defined response procedures, and response SLAs were documented.

Vulnerability Management Process Redesign

We replaced the annual testing model with a continuous vulnerability management process. Authenticated scanning runs on a defined schedule. Newly discovered vulnerabilities are triaged within 24 hours and remediation windows are tracked against severity classification. The process is documented, owned, and generates evidence that can be presented to a QSA.

Documentation Remediation

Every policy document was revised to match the actual technical implementation. Where the implementation was the correct approach but the documentation was outdated, we updated the documentation. Where the documentation described a control that was superior to the implementation, we chose to implement to the documented standard.

The output at Day 60: All 47 gap items remediated and in evidence-collection state.

Phase 3 (Days 61–90): Evidence Preparation and Pre-Assessment Validation

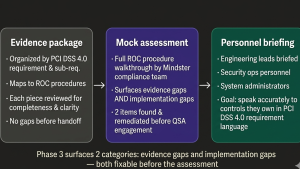

An assessment-ready state is not the same as a remediated state. QSA assessments require organized, labelled evidence packages, clear audit trails, and personnel who can speak to controls during interviews. Phase 3 addresses this.

What happened:

- Evidence collection and organization by requirement domain

- Internal validation testing: each control was independently tested against the PCI DSS 4.0 requirement wording

- Mock assessment: Mindster’s compliance team conducted a structured walkthrough using the PCI DSS v4.0 ROC (Report on Compliance) procedures

- Remediation of any items identified during mock assessment

- Briefing of client personnel who would be interviewed during the QSA assessment

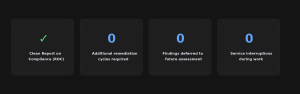

The output: A complete evidence package, organized by PCI DSS 4.0 requirement, with no gaps requiring further remediation.

The result

The client completed its PCI DSS 4.0 assessment within the required timeline and received a clean Report on Compliance from the QSA.

More importantly, the engagement established operational security processes that remained active beyond the assessment cycle:

- MFA governance became part of standard infrastructure operations

- Vulnerability management shifted from annual testing to continuous remediation workflows

- Monitoring and alerting became integrated into day-to-day security operations

- Compliance evidence generation became structured and repeatable

- Documentation governance was aligned with change management processes

The outcome was not only assessment readiness, but a more resilient payment security operating model.

What This Engagement Demonstrates About PCI DSS 4.0 Readiness

Based on this engagement and others in the fintech sector, three things consistently determine whether a 90-day compliance programme succeeds or fails.

Gap assessment quality determines everything downstream:

If the gap assessment is incomplete or politically softened — if your team marks items green because remediation would be expensive — the assessment will fail. Accurate gap identification is the most important work of the entire programme.

Technical implementation must be validated against requirement wording, not against intent:

PCI DSS 4.0 requirements are specific. A monitoring implementation that captures 90% of the required event categories does not satisfy the requirement. Engineers remediating compliance gaps need to work from the requirement text, not a summary interpretation.

Documentation and implementation must match:

The gap between what your policies say and what your systems do is one of the most common assessment failures. This gap is fixable. It requires discipline, not complexity.

The Compliance Window for PCI DSS 4.0 Is Now

The March 2024 enforcement date has passed. Any organization processing card payments and operating under a PCI DSS assessment cycle is now being assessed against version 4.0.

If your last assessment was under version 3.2.1, your next one will identify gaps in your MFA architecture, your monitoring framework, and your documentation alignment — unless you have already addressed them.

A 90-day remediation programme is achievable for most fintech organizations. The variable is whether the programme is structured and resourced properly from the start.

Mindster’s structured engagement model for PCI DSS 4.0

Every engagement follows the same sequenced approach. The order matters — shortcuts taken in the early phases consistently cause failures in the later ones.

How Mindster Works With Fintech Brands on Compliance

Mindster has built fintech payment platforms and compliance-critical systems for clients operating across regulated financial markets. The C3Pay engagement — where we built the UAE’s largest WPS-compliant salary processing platform for Edenred, serving over 1.6 million active users — is one example of how we approach regulated fintech engineering: compliance is built into the architecture, not added after the fact.

PCI DSS 4.0 compliance work follows the same principle. Controls are implemented to hold, not to pass an audit.

If you are approaching a QSA assessment or want to assess your current compliance posture against PCI DSS 4.0 requirements, our fintech engineering and compliance team can scope a gap assessment within a week.

Talk to Mindster’s Fintech Team →

Frequently Asked Questions

1.What is the difference between PCI DSS 3.2.1 and PCI DSS 4.0?

PCI DSS 4.0 introduced stricter multi-factor authentication requirements, mandatory automated monitoring, continuous vulnerability management processes, and a customized implementation pathway that requires documented rationale. It shifted from point-in-time validation to continuous control assurance.

2.Is PCI DSS 4.0 now mandatory?

Yes. PCI DSS 4.0 became the mandatory standard in March 2024. All QSA assessments are now conducted against version 4.0.

3.Can PCI DSS 4.0 compliance realistically be achieved in 90 days?

For organizations that have an existing compliance posture built against version 3.2.1, a structured 90-day programme is achievable. The key variable is the quality of the initial gap assessment and the availability of dedicated engineering and compliance resources during the remediation phase.

4.What is the biggest compliance gap Mindster finds in fintech organizations?

Consistently, the largest gap is misalignment between written documentation and actual technical controls. Organizations that allow their policy documentation to drift from their live implementation face significant remediation work before a QSA assessment can proceed.

5.Does Mindster provide ongoing compliance support after the assessment?

Yes. We work with clients to ensure that controls implemented during a remediation programme are maintained as operational processes, not treated as one-time tasks. This includes vulnerability management process ownership, monitoring configuration maintenance, and documentation update procedures.

Mindster is a fintech product engineering company with experience building and securing payment platforms across regulated financial markets. Our fintech solutions practice covers product development, security architecture, and compliance engineering for card payment and digital wallet systems.

Akhila drives the content strategy at Mindster, combining analytical clarity with a passion for digital product innovation. With a deep focus on mobile app strategy and software solutions, she bridges the gap between engineering complexity and intuitive user experiences. She thoughtfully articulates tech concepts, transforming frameworks, case studies, and digital transformation trends into actionable insights for product teams and business leaders.