When Mindster’s engineering team began building C3Pay for Edenred UAE — a payroll platform that would process salaries for 2 million migrant workers across the GCC — the first architectural decision had nothing to do with features. It was about a boundary: which services are allowed to touch salary data, and what happens when that boundary is violated.

The answer was not theoretical. Get it wrong — let transaction records share a database with a general-purpose application layer, or let a remittance API carry raw account identifiers that a logging sidecar can read — and the entire backend falls under UAE Central Bank audit scope simultaneously. At 1.6 million active users processing time-critical WPS payroll, you cannot stop the platform to remediate a structural design error.

The Core Thesis of Payment Engineering

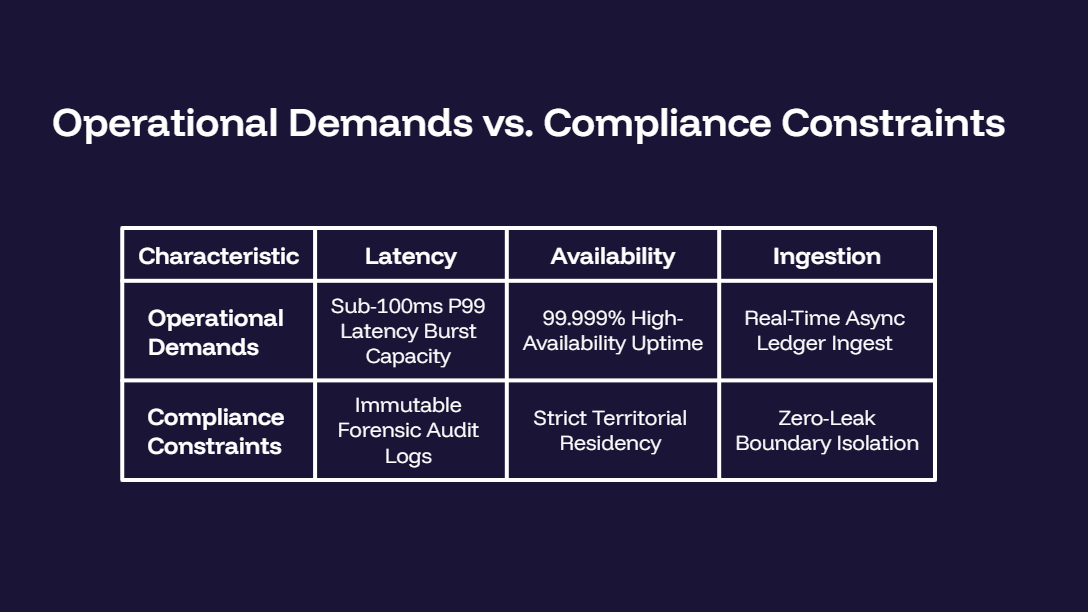

The system must sustain high transaction volumes with low latency and near-perfect uptime while satisfying compliance frameworks that impose hard constraints on how data flows, where it lives, and who can touch it.

Most teams hit a wall not because they ignored compliance, but because they deferred it. When internal services skip mutual TLS, or logs capture raw account numbers, every component inherits audit scope. Remediation at that point costs 3–5× what correct isolation would have cost at design time.

The architectural answer is isolation through abstraction: compliance-sensitive data and logic are confined behind narrow service interfaces. The product layer operates entirely on tokens—never on raw financial credentials.

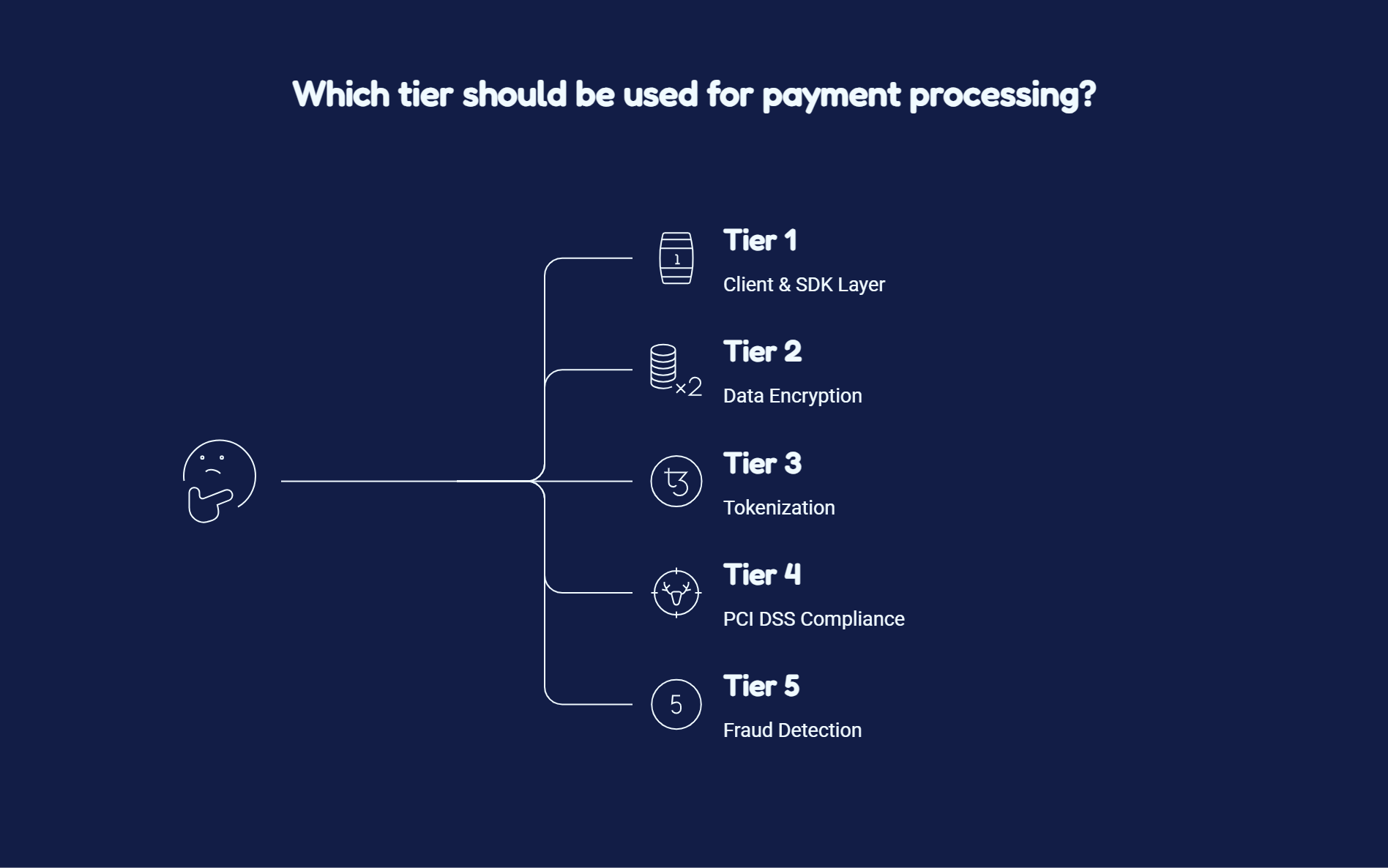

2. Core Architectural Components of a Regulated Payment System

A compliant payment engine is not a monolith with security middleware added on top. It is five isolated service tiers, each with a single compliance responsibility, communicating through APIs that carry no raw financial credentials.

When PAN data, session state, routing logic, and financial ledgers share a database, the audit perimeter expands to every service touching that database — including logging sidecars, analytics pipelines, and CI/CD jobs. Every schema migration, dependency upgrade, or feature rollout now requires change-management documentation and QSA review eligibility. The deployment pipeline stops being a product tool and becomes a compliance gate.

The structural solution is strict tier isolation:

| ACTIVE SELECTION SCHEMA DETAILS:

Tier 1: Client & SDK Layer

Tier 1 is the only place raw card data should exist. A hosted iFrame or mobile SDK submits the PAN directly to a PCI-compliant tokenization vault. Your servers receive an opaque token. If you build a custom form that passes a raw PAN through your API — even as a transient value captured at DEBUG log level — your entire backend enters PCI scope. Every server, every engineer, every deployment pipeline inherits the full weight of PCI DSS Requirements 1, 3, 7, and 10.

Tier 2: API Gateway

Tier 2 must run in blocking mode, not detection mode. PCI DSS v4.0 Requirement 6.4.2 is explicit: detection-only WAF is a non-compliant control. Rate limiting must operate at the payment_method_token and merchant_id dimensions — not just IP address — because denial-of-wallet attacks rotate IPs while reusing valid token references, each triggering downstream processor calls and fraud scoring at per-call cost.

Tier 3: Orchestration State Machine

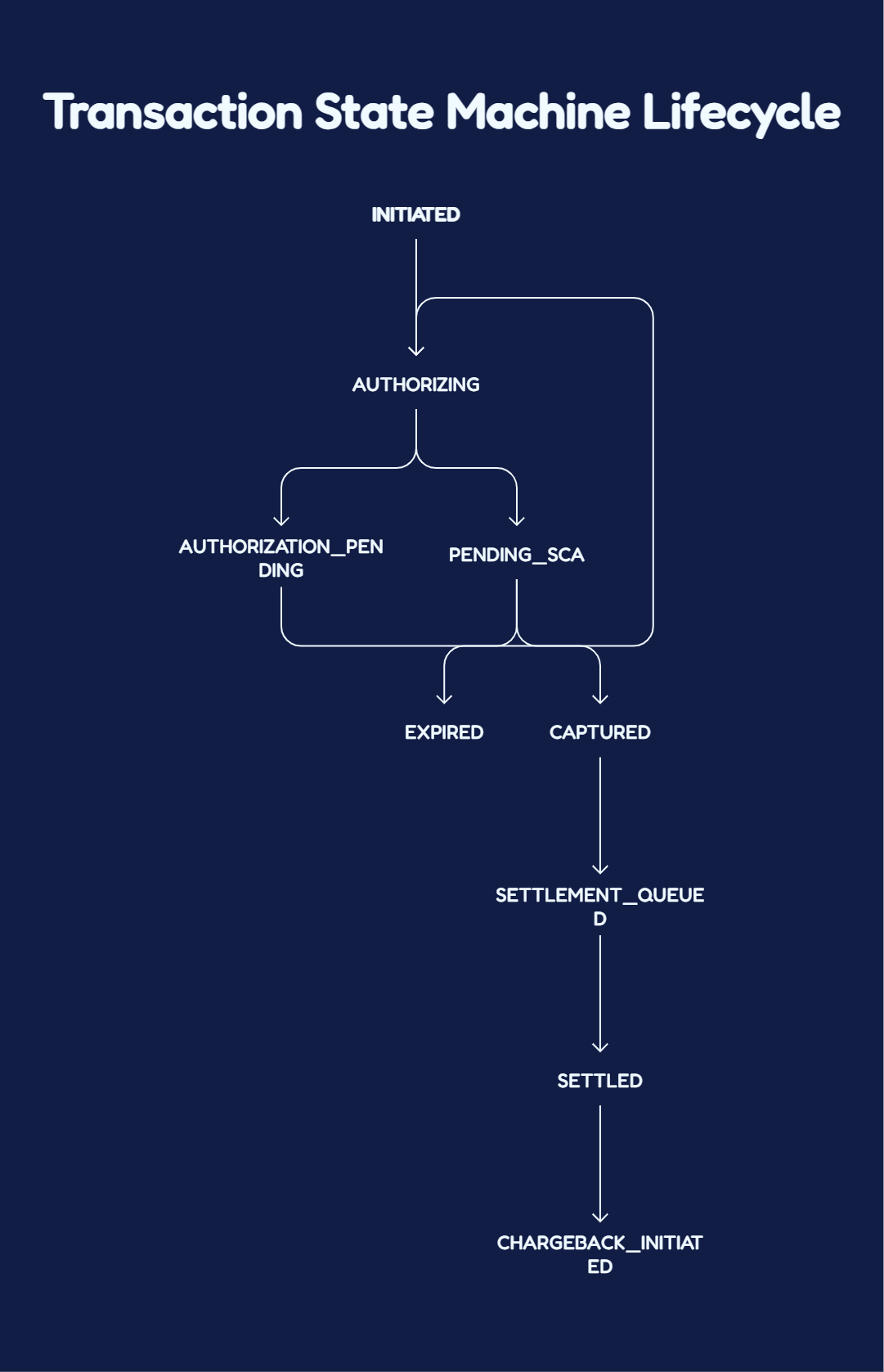

Tier 3 handles transaction lifecycle as a finite state machine with idempotent, replayable transitions. Network timeouts, processor partial failures, and SCA redirects create re-entrant execution paths. A sequence of database flag updates cannot safely handle them.

Tier 4: Ledger Engine

Tier 4 stores money movement as append-only double-entry records. Balances are derived at read time from ledger entries — they are never stored as a column that can be directly modified. Amounts are stored in minor currency units (integer pence, fils, paise) to eliminate floating-point rounding errors that compound into reconciliation failures at scale.

Tier 5: Risk & Compliance

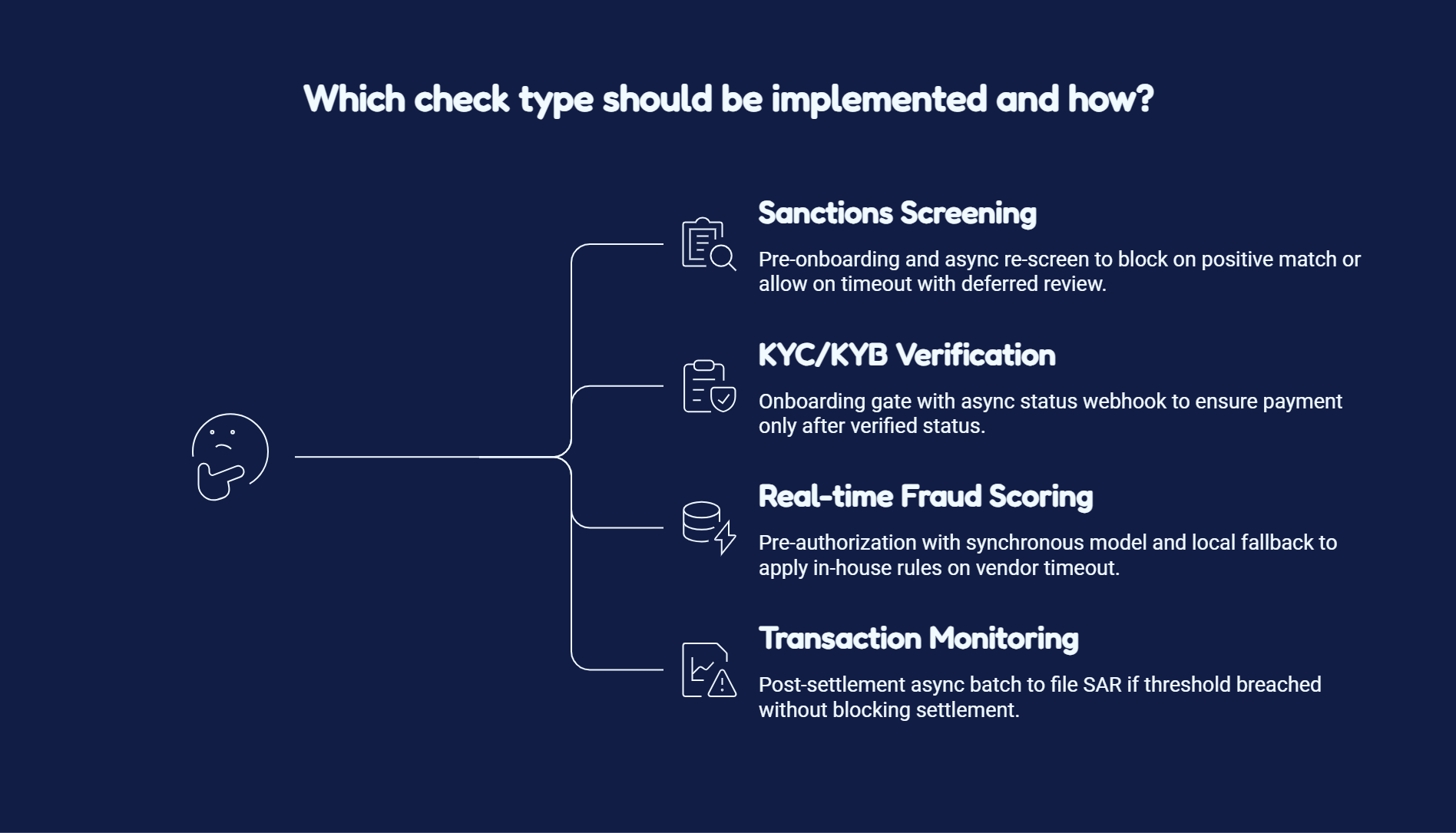

Tier 5 runs compliance checks outside the main transaction path. Synchronous coupling to a third-party AML or fraud vendor means their P99 latency spike becomes your checkout timeout.

CRITICAL ARCHITECTURAL CONSTRAINTS

-

PCI CDE SCOPE: Strictly confined to Tier 1 vault + Tier 4 ledger environments.

-

PRODUCT LAYER VELOCITY: Tiers 2–3 iterate completely without triggering continuous CDE review cycles or deployment locks.

[ COMPONENT: ACCENTED EVIDENCE CALLOUT CARD ]

🏗️ What Mindster built — ONEIC, Oman

ONEIC is Oman’s largest licensed Non-Banking Financial Institution and Payment Service Provider. Mindster implemented KYC as a pure onboarding gate using Uqudo’s biometric identity service against Central Bank of Oman national databases — completely outside the payment flow.

A new user completes identity verification before wallet activation. The payment path never waits on the compliance check; the compliance check gates access to the payment path.

The result: 80% automated onboarding with 500,000+ active wallet users and zero KYC bottleneck in the live transaction loop.

Why Monolithic Payment Architectures Fail Audits

| Tier | Name | Core Function | PCI Scope Impact |

|---|---|---|---|

| 1 | Client & SDK Layer | Hosted iFrame / Mobile SDK captures PAN directly to vault. App receives opaque payment_token only. | OUT OF SCOPE — PAN never touches app servers |

| 2 | API Gateway & Routing Edge | mTLS termination, JSON schema validation, rate limiting, WAF enforcement, OAuth token introspection. | OUT OF SCOPE — forwards tokens, not PANs |

| 3 | Orchestration State Machine | Stateless FSM managing state transitions (INITIATED → AUTHORIZING → CAPTURED → SETTLED). Idempotent key enforcement. | OUT OF SCOPE — references tokens, not card data |

| 4 | Ledger Engine | Append-only double-entry bookkeeping. No UPDATE/DELETE on committed entries. WORM-equivalent storage. | IN SCOPE — financial source of truth |

| 5 | Risk & Compliance Tier | AML sanctions screening, KYC/KYB verification, real-time fraud scoring. Decoupled from main transaction loop. | OUT OF SCOPE — operates on reference IDs |

Tier 1 — The Client & SDK Layer

Raw PANs and CVVs must be captured on the client device and submitted directly to a PCI-compliant tokenization vault — bypassing your application servers entirely — so that your backend infrastructure never enters CDE scope.

- iFrame origin rule: The iFrame origin must be the vault provider’s domain. Any proxying through your servers re-introduces CDE scope.

- CSP headers: Explicitly allowlist the vault domain and block all other frame sources.

- Certificate pinning: Mobile SDKs must implement certificate pinning against the vault’s TLS certificate chain to prevent MITM interception.

- Token response: Strip expiry date and CVV before passing upstream. Only last-four and token reference are safe to persist in the application database.

| COST OF FAILURE

A single custom-built form that allows a raw PAN to pass through your API — even as a transient in-memory value logged at DEBUG level — places your entire backend fleet in PCI DSS scope. Remediation means Requirement 1, 3, 7, and 10 apply to every server in your infrastructure. |

Tier 2 — The API Gateway & Routing Edge

The API gateway must terminate mTLS, enforce strict request schema validation, and apply rate limiting at the edge before any payload reaches an internal microservice. This is the primary control point for PCI DSS v4.0 Requirement 6.4 (web-facing application protection) and Requirement 8.6 (service account authentication).

| Cluster Article Candidate

The gateway’s mTLS certificate lifecycle management — rotation schedules, SPIFFE/SPIRE-based workload identity, and integration with cert-manager in Kubernetes — warrants a dedicated deep-dive: Zero-Trust Service Mesh Architecture for Payment Systems. |

Tier 3 — The Orchestration State Machine

Payment transaction lifecycle must be modeled as an explicit finite state machine with idempotent, externally-replayable transitions — not as a sequence of conditional database flag updates — because network timeouts, processor partial failures, and SCA redirects create re-entrant execution paths that mutable flag logic cannot safely handle.

| Cluster Article Candidate

The idempotency key architecture — including distributed lock design with Redis Redlock, database-level deduplication schema, and safe retry windows for processor callbacks — is covered in: Deep Dive: Implementing Redis-Backed Idempotency for Payment APIs. |

Tier 4 — The Ledger Engine

The financial ledger must be implemented as an append-only, double-entry bookkeeping system stored in WORM-equivalent database rows — no UPDATE or DELETE operations on committed entries — because mutable ledger state cannot satisfy SOX Section 404 tamper-evidence requirements, PCI DSS v4.0 Requirement 10.3.3, or DORA Article 9 integrity controls.

| Cluster Article Candidate

Ledger schema design — partitioning strategy, read-model materialization, and database-level double-entry constraints — is covered in: Designing an Immutable Double-Entry Ledger Schema for Payment Systems. |

Tier 5 — The Risk & Compliance Tier

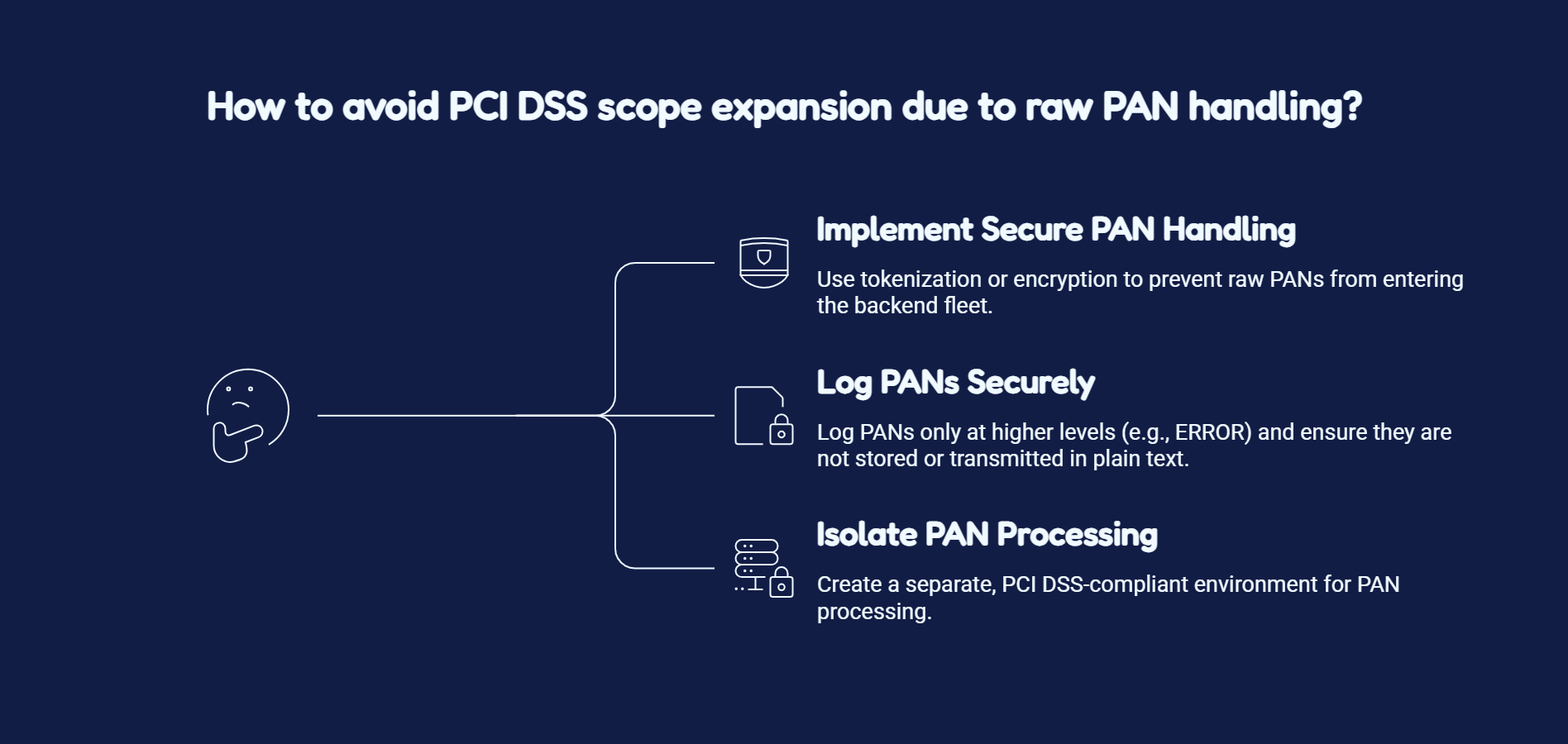

AML sanctions screening, KYC/KYB verification, and real-time fraud scoring must execute in services that are fully decoupled from the core payment routing loop. Synchronous coupling to third-party compliance APIs introduces availability dependency that directly maps to payment gateway uptime.

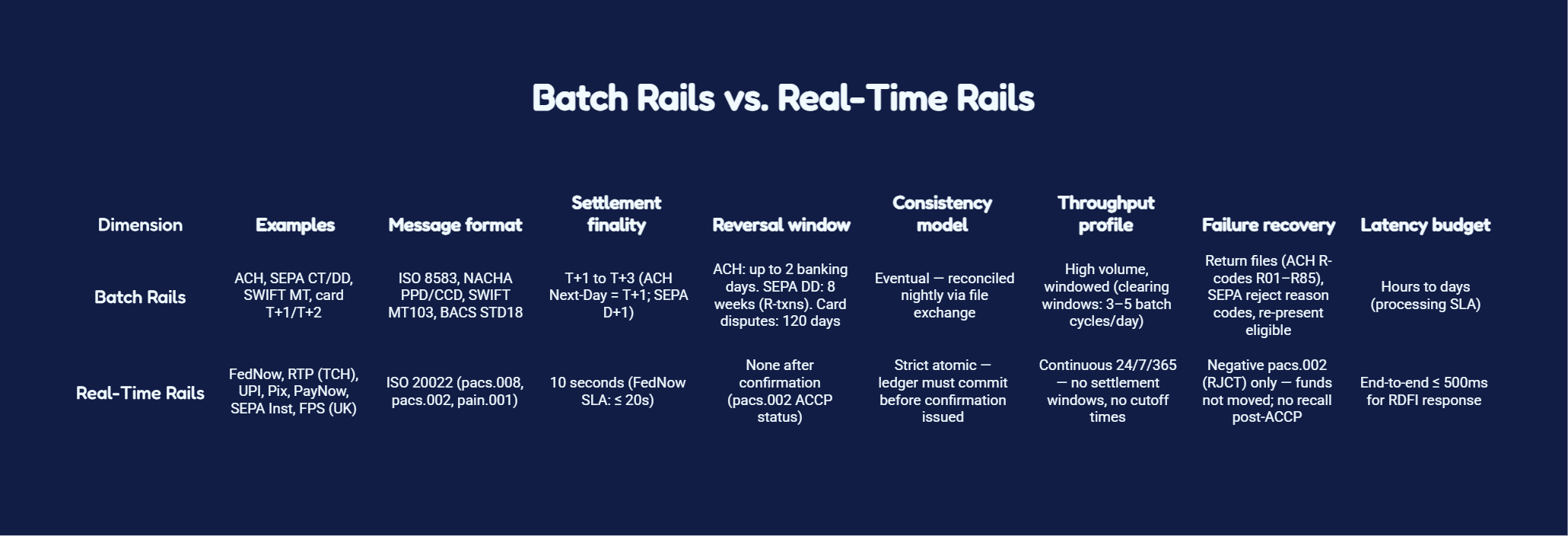

3. The Anatomy of a Transaction Lifecycle: Batch Processing vs. Real-Time Rails

The architectural gap between batch payment rails and real-time payment networks is not a performance optimization problem — it is a fundamentally different consistency contract: batch rails tolerate eventual consistency across multi-day clearing windows, while real-time rails demand atomic, irreversible finality within 500ms, with zero application-layer opportunity to correct an error after settlement confirmation is issued.

The Two Settlement Contracts

Asynchronous Batch Processing: ACH, SEPA, and File-Exchange Rails

Batch payment rails operate on a file-exchange model where transactions are aggregated into ISO 8583 or ISO 20022 message files, submitted to a clearing house within defined settlement windows, and reconciled against return files — making multi-day eventual consistency not a system flaw but an explicit contractual property of the network.

| COST OF FAILURE — NOC PROCESSING

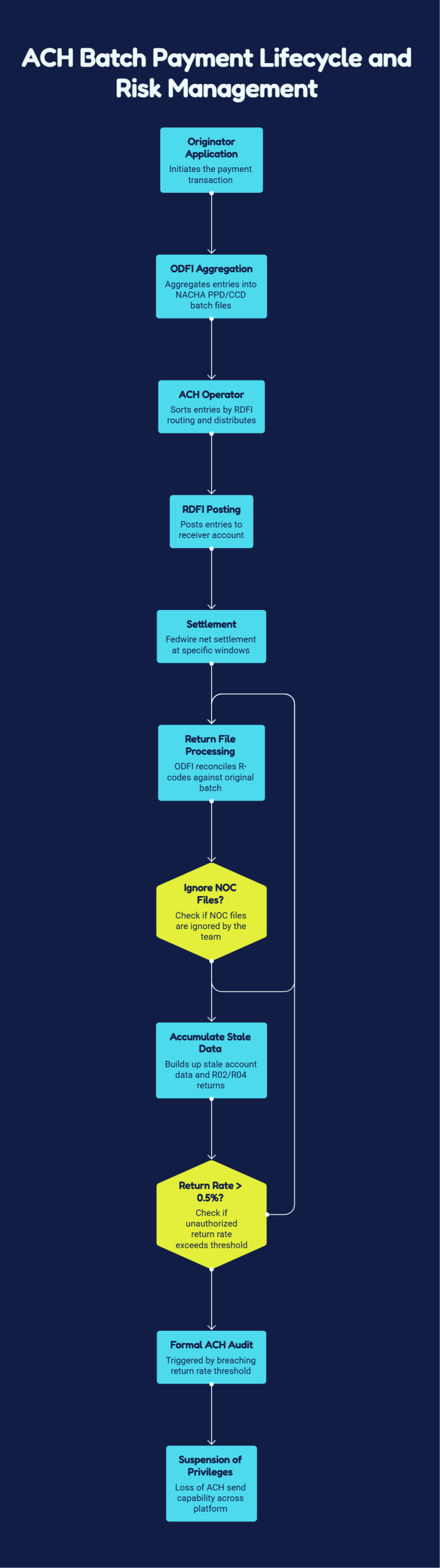

Teams that process settlement and return files but ignore NOC files (COR/C01–C09 entries) accumulate stale account data, generating compounding R02 and R04 return rates. NACHA’s return rate threshold for unauthorized returns is 0.5% — breaching it triggers a formal ACH audit and, at persistent violation, suspension of ODFI origination privileges. That is not a technical warning; it is the loss of ACH send capability across your entire platform. |

Real-Time Payment Rails: Engineering for Instant Finality

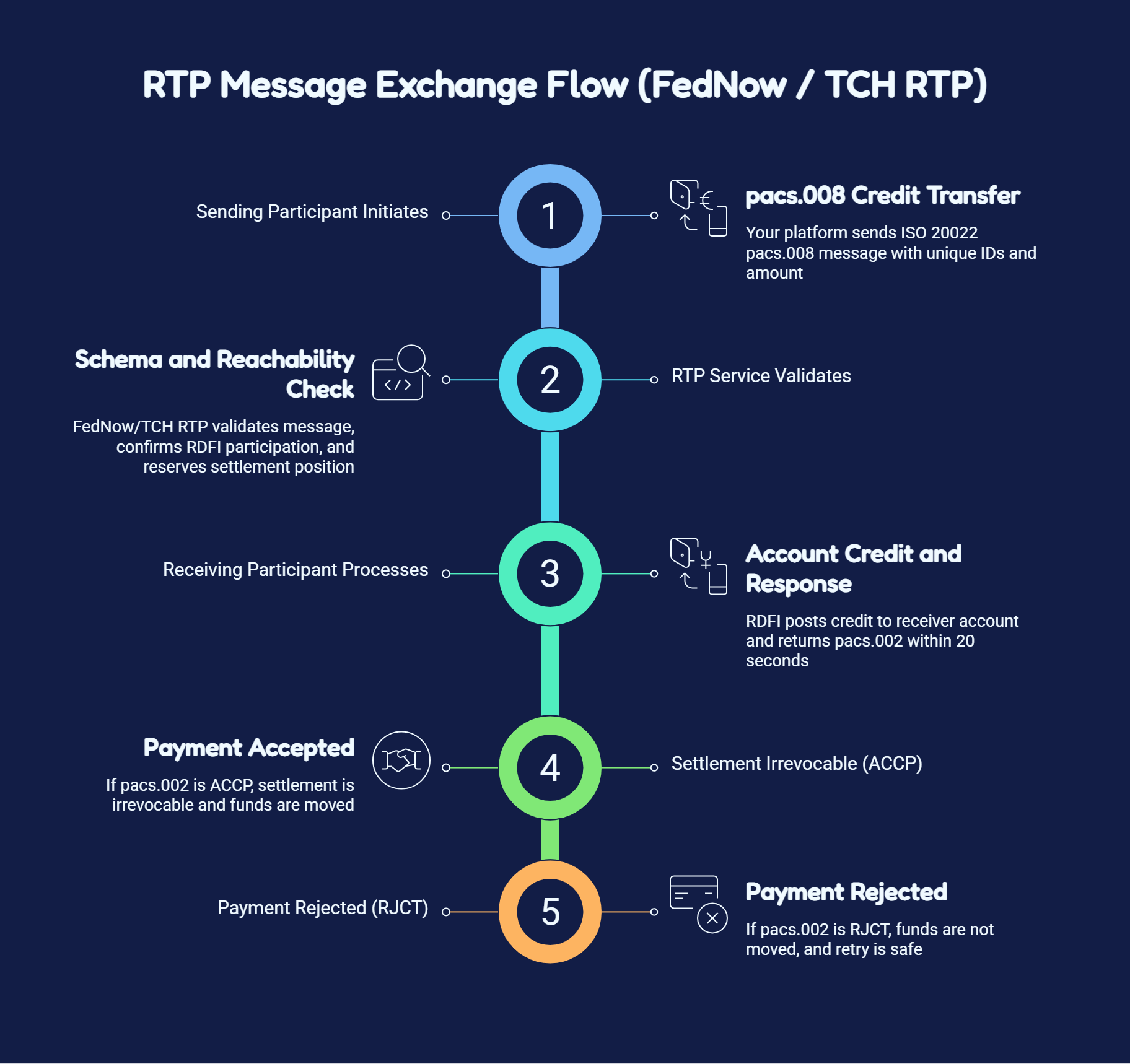

Real-time payment networks — FedNow, TCH RTP, Brazil’s Pix, India’s UPI — operate on ISO 20022 pacs.008/pacs.002 message exchanges with sub-10-second end-to-end settlement finality. The receiving institution’s pacs.002 ACCP response is legally and operationally irrevocable: there is no R-code, no return window, and no network-layer mechanism to recall a settled payment.

Database Concurrency Strategies for Atomic Balance Updates

Real-time payment ledger writes require either pessimistic locking via SELECT FOR UPDATE or optimistic locking via version-column compare-and-swap. The choice is determined by your read/write contention profile — pessimistic locking serializes concurrent debits safely but degrades throughput on hot accounts; optimistic locking scales under low contention but generates retry storms on high-frequency accounts.

| Strategy | Mechanism | When to Use | Risk of Getting It Wrong |

|---|---|---|---|

| Pessimistic locking | SELECT FOR UPDATE — acquires exclusive row lock before reading balance | Accounts with high concurrent debit frequency (e.g., merchant settlement accounts) | Hot accounts create a write queue. At 1,000 concurrent RTP debits, lock wait time dominates latency. Cascades to retry storms and throughput collapse. |

| Optimistic locking | Version-column CAS — UPDATE WHERE version = N; check rows affected | Low-to-moderate concurrent write frequency; architectures with account sharding | Under high contention, version conflicts produce livelock — all writers retrying indefinitely, none committing, until connection pool exhaustion triggers circuit breaker. |

| Balance reservation | Redis DECRBY (atomic) on available_balance key with TTL for expiry | Hot accounts at RTP scale; platforms with mixed cold/hot account profiles | Consistency gap between Redis balance and ledger balance. Silent async writer failure → stale Redis balance → customer can spend money already spent. |

| Cluster Article Candidate

The full treatment of database concurrency — PostgreSQL advisory locks, CockroachDB serializable isolation, account sharding to eliminate hot-row contention, and event-sourced balance derivation vs. materialized snapshot models — is covered in: Database Concurrency Strategies for Real-Time Financial Ledgers. |

4. Mapping Regulatory Frameworks to Engineering Requirements

Regulatory frameworks are not policy documents to be handed to a legal team — they are engineering specifications that dictate network topology, database schema constraints, API contract design, cryptographic key custody, and runtime access control models. Treating them otherwise produces the most expensive class of architectural debt: compliance-driven rework discovered during a QSA audit or regulatory examination, executed under deadline pressure, against a production system that was never designed to accommodate the required isolation.

| Regulation | Technical Scope | Architectural Requirement | Cost of Failure |

|---|---|---|---|

| PCI DSS v4.x — Req. 1 & 2 | Network segmentation; CDE boundary definition | Dedicated VPC/VLAN for all CDE components; default-deny firewall rules; no lateral reachability from general application subnets; quarterly firewall rule review logged and signed | Full infrastructure re-scoping under QSA assessment. Every server reachable from CDE enters scope, multiplying SAQ-D line items across the entire fleet. |

| PCI DSS v4.x — Req. 3 | PAN storage and protection | FPE or tokenization for any PAN at rest; HSM-backed key custody (FIPS 140-2 Level 3 minimum); key rotation ≤ 1 year; cryptographic key inventory maintained | A single unencrypted PAN in a log file triggers a reportable data breach. Visa/Mastercard forensic investigation (PFI) costs begin at $20K–$100K before remediation, fines, or card reissuance liability. |

| PCI DSS v4.x — Req. 4 | Encryption in transit across all CDE communication paths | TLS 1.2 minimum (TLS 1.3 preferred); mTLS for all internal CDE service-to-service calls; explicit prohibition of SSL, TLS 1.0, TLS 1.1, and weak cipher suites (RC4, 3DES, export-grade) | A single service-to-service call using a deprecated protocol is a direct Requirement 4 finding. Compensating controls must be formally documented and accepted by the QSA — expensive alternative to enforcing TLS 1.2+ at platform level. |

| PCI DSS v4.x — Req. 6.4 | Web-facing application security | WAF enforcing OWASP CRS 3.3+ in blocking mode (not detection-only) on all CDE-adjacent endpoints; automated DAST in CI/CD pipeline; penetration test annually and after significant changes | Detection-mode WAF is non-compliant under v4.0 Requirement 6.4.2. A failed Req. 6.4 control pauses SAQ-D or ROC issuance until remediated. |

| PCI DSS v4.x — Req. 10 | Audit log integrity, retention, and tamper evidence | Append-only audit log storage (WORM-equivalent: S3 Object Lock or SIEM with write-once indexing); retention ≥ 12 months; logs capture user ID, event type, date/time, success/failure, originating IP; integrity verified by cryptographic hash | Mutable log storage is an automatic Requirement 10.3.3 finding. In a breach, tampered logs eliminate forensic reconstruction capability — maximizing card brand fine exposure and card reissuance liability. |

| PSD3 / Open Banking — SCA | Strong Customer Authentication for payment initiation | SCA must satisfy 2-of-3 factor authentication (possession + knowledge + inherence) per EBA RTS; dynamic linking required — authentication code bound to specific transaction amount and payee; SCA exemptions tracked per bucket with exposure counters | Static OTP without dynamic linking is PSD2/PSD3 RTS non-compliance. Incorrectly applied SCA shifts chargeback liability for all disputed transactions from issuer to PSP. |

| PSD3 / Open Banking — TPP Access | Third-Party Provider API access and consent management | Dedicated API gateway for TPP traffic; OAuth 2.0 with PKCE; fine-grained scopes (accounts:read, payments:initiate:single, payments:initiate:recurring); consent object persisted with granted scopes, expiry, TPP identifier, customer reference; revocation propagated within SLA | Coarse-grained OAuth scopes violate GDPR Article 5(1)(c) data minimization. Over-privileged TPP access consents are enforceable by NCA sanction — fines up to 4% of global annual turnover under GDPR Article 83(5). |

| GDPR / Data Sovereignty — Localization | Personal data residency and cross-border transfer controls | Regional data plane isolation: separate database clusters per data residency zone (EU, IN, US); transaction records containing personal data must not replicate across jurisdictional boundaries without valid transfer mechanism (SCCs, adequacy decision, BCRs) | Cross-border transfer of EU personal data to a non-adequate country without valid transfer mechanism is a GDPR Article 46 violation — enforceable at up to 4% of global annual turnover (Article 83(5)). |

| GDPR — Right to Erasure | Data subject erasure obligations vs. financial record retention | Pseudonymization-first architecture: PII stored in dedicated identity service; transaction records reference only a customer_reference_id (opaque UUID); erasure request deletes PII from identity service, leaving ledger records intact but unlinked | Storing PII directly in transaction ledger rows makes erasure structurally impossible without corrupting the financial audit trail — a direct conflict between GDPR Article 17 and financial record retention obligations under AML law. |

| AML / CFT — Sanctions Screening | OFAC SDN, UN Consolidated, EU Consolidated, HMT screening | Sanctions screening service integrated as a pre-authorization gate — executes before any ledger mutation or pacs.008 dispatch; screening covers originator, beneficiary, and referenced parties; positive match → freeze and file SAR/STR | Executing a payment to a sanctioned entity is a potential OFAC strict liability violation. Civil penalties: up to the greater of $1M or twice the transaction value. Debarment from US dollar correspondent banking relationships is commercially existential. |

| AML / CFT — KYC/KYB | Identity verification and beneficial ownership at onboarding | KYC pipeline: document verification + database screening (PEP, adverse media, sanctions) + risk scoring. KYB: UBO resolution to natural person level (≥ 25% ownership threshold, FATF Rec. 24); ongoing re-KYC on schedule | Onboarding without completing required KYC/KYB is a BSA Section 352 violation. For payment facilitators, liability extends to sub-merchants — Mastercard and Visa PF agreements explicitly assign this liability to the facilitator. |

| RBI / Local Central Bank Mandates | Data localization for domestic payment transactions | For India (RBI Storage Circular, 2018): all payment system data must be stored exclusively in India; no mirroring or processing abroad; foreign card networks must comply or obtain explicit RBI exemption | Retrofitting regional isolation requires re-architecting data replication topology, adding latency to cross-region reads, and potentially re-issuing all tokens generated outside the mandated region — a multi-month program executed under regulatory deadline, with payment license suspension as backstop. |

Control Interaction Conflicts

The harder engineering problem is control interaction: GDPR’s right to erasure directly conflicts with AML’s 5-year transaction record retention obligation. PSD3’s TPP access requirements mandate data sharing that GDPR’s data minimization principle requires you to restrict. These conflicts are resolved by architecture:

| Conflict | Architectural Resolution |

|---|---|

| GDPR erasure vs. AML retention | Pseudonymization at ingestion: delete PII, retain ledger rows unlinked |

| PSD3 data sharing vs. GDPR data minimization | Scope-bounded consent objects; TPP access limited to granted scopes with expiry enforcement |

| PCI log retention vs. GDPR purpose limitation | PII scrubbing in log pipeline before write to SIEM/aggregator |

| RBI localization vs. global active-active architecture | Regional data plane isolation; no cross-border replication of in-scope payment data fields |

| Cluster Article Candidate

The PSD3 SCA and consent lifecycle engineering problem — dynamic linking, exemption bucket tracking, TPP consent schema design, and OAuth 2.0 scope architecture for Open Banking APIs — is covered in: Navigating PSD3: Engineering Consent Lifecycles and SCA APIs. |

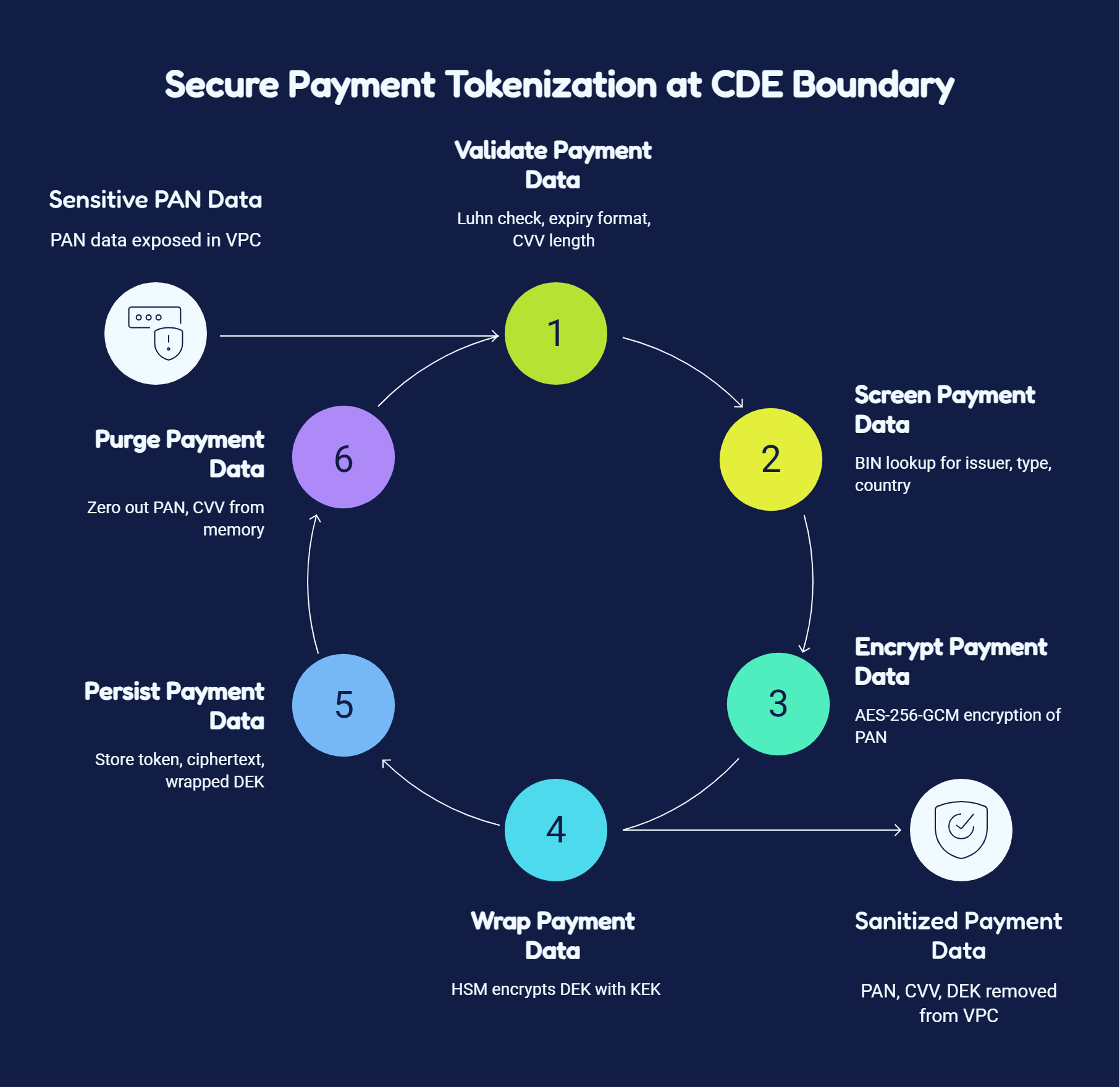

5. Isolation & Data Sovereignty: Designing the CDE and Geo-Sharded Layers

CDE isolation and geo-sharded data residency are not deployment configurations — they are structural architectural decisions that must be resolved at network topology design time, because retrofitting either pattern onto a running payment system requires re-architecting data flows, re-issuing tokens, migrating live database clusters across jurisdictional boundaries, and re-scoping a PCI audit from scratch, all simultaneously, under regulatory deadline.

CDE Network Architecture

The CDE must be implemented as a physically separate network segment — a dedicated VPC or VLAN with explicit, default-deny ingress and egress rules — where the only permitted inbound connections originate from the tokenization service’s specific subnet, and the only permitted outbound connections terminate at the HSM or cloud KMS endpoint and the card scheme authorization network.

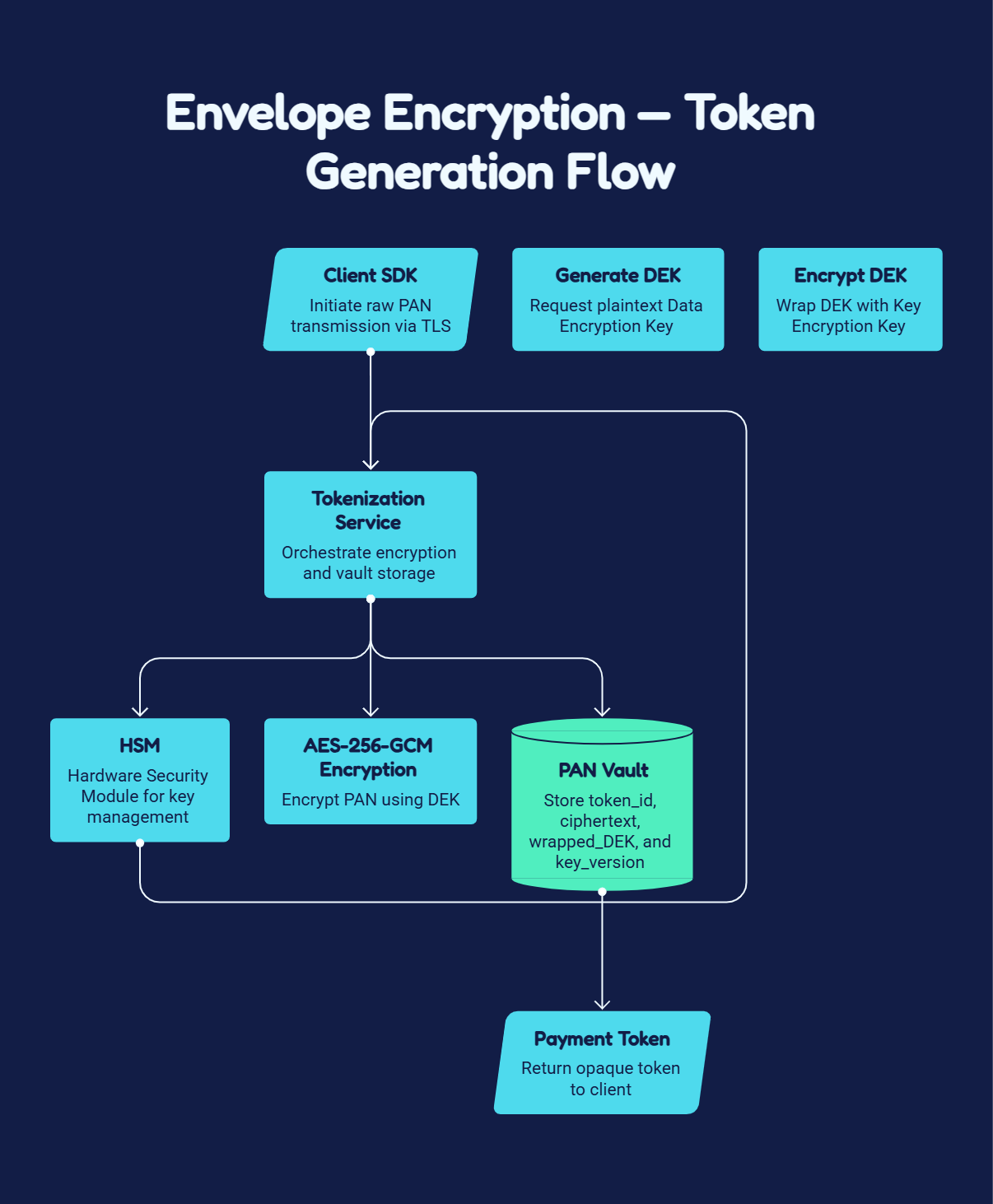

Tokenization Vault: Envelope Encryption

A tokenization vault replaces raw PANs with cryptographically opaque token strings using envelope encryption — where the PAN is encrypted with a Data Encryption Key (DEK) that is itself encrypted with a Key Encryption Key (KEK) stored exclusively in an HSM — so that the vault datastore contains only ciphertext that is useless without HSM access, and the HSM contains only key material with no access to the data it protects.

| HSM Option | FIPS Certification | Key Operations | Operational Considerations |

|---|---|---|---|

| AWS CloudHSM | FIPS 140-2 Level 3 | RSA, AES, EC, PKCS#11 | Single-tenant; customer-managed key material; higher operational overhead than KMS |

| AWS KMS (Custom Key Store) | FIPS 140-2 Level 3 (via CloudHSM backing) | AES-256, RSA 2048/4096 | Managed service; lower ops overhead; key material never leaves HSM boundary |

| Thales Luna Network HSM 7 | FIPS 140-2 Level 3 / Level 4 | Full PKCS#11, JCE, CNG | On-premises or colocation; required for some central bank mandates that prohibit cloud key custody |

| nCipher nShield Connect | FIPS 140-2 Level 3 | PKCS#11, OpenSSL engine | Strong hardware attestation; supports Security World key sharing across HSM cluster |

| COST OF FAILURE — KEY MATERIAL EXPOSURE

Storing KEK material in application configuration files, environment variables, or AWS Parameter Store (standard tier) is a Requirement 3.7 finding. Remediation requires rotating all KEKs, re-wrapping all DEKs, auditing all systems that may have accessed the exposed key material, and notifying card brands — a process that typically runs 60–90 days and consumes the equivalent of a full engineering team sprint. |

Payload Sanitization: The Tokenization Boundary

Geo-Sharded Databases: Satisfying Data Localization

Data localization mandates require that transaction records containing personal data be stored and processed exclusively within defined geographic boundaries. At global platform scale this requires a geo-sharded database architecture where each regional shard is a fully independent data plane with no cross-border replication of in-scope fields.

| COST OF FAILURE — GLOBAL REPLICATION

A global database architecture with multi-region replication that copies EU resident transaction records to a US region is a GDPR Article 46 violation if no valid transfer mechanism is in place. Post-Schrems II, Standard Contractual Clauses require a Transfer Impact Assessment. The engineering cost of retrofitting geo-sharding onto a previously global database is measured in months of migration work — all while maintaining 99.999% availability for live payment processing. |

| Cluster Article Candidate

The full engineering treatment of geo-sharded ledger design — covering shard key selection, CockroachDB vs. Vitess vs. Citus for regional partitioning, zero-downtime cross-shard migration procedures, and the pseudonymized global aggregate pipeline — is covered in: Architecting Geo-Sharded Ledgers for Localization Compliance. |

6. Resiliency and Reliability: Preventing Double Charges and Outages

In payment systems, the failure modes that cause the most commercial damage are not crashes or data corruption — they are silent correctness violations: a retry that charges a customer twice, an event that fails to publish after a ledger commit, a processor failover that loses the authorization state of an in-flight transaction. These failures are invisible until they surface as chargeback disputes, reconciliation breaks, or regulatory findings.

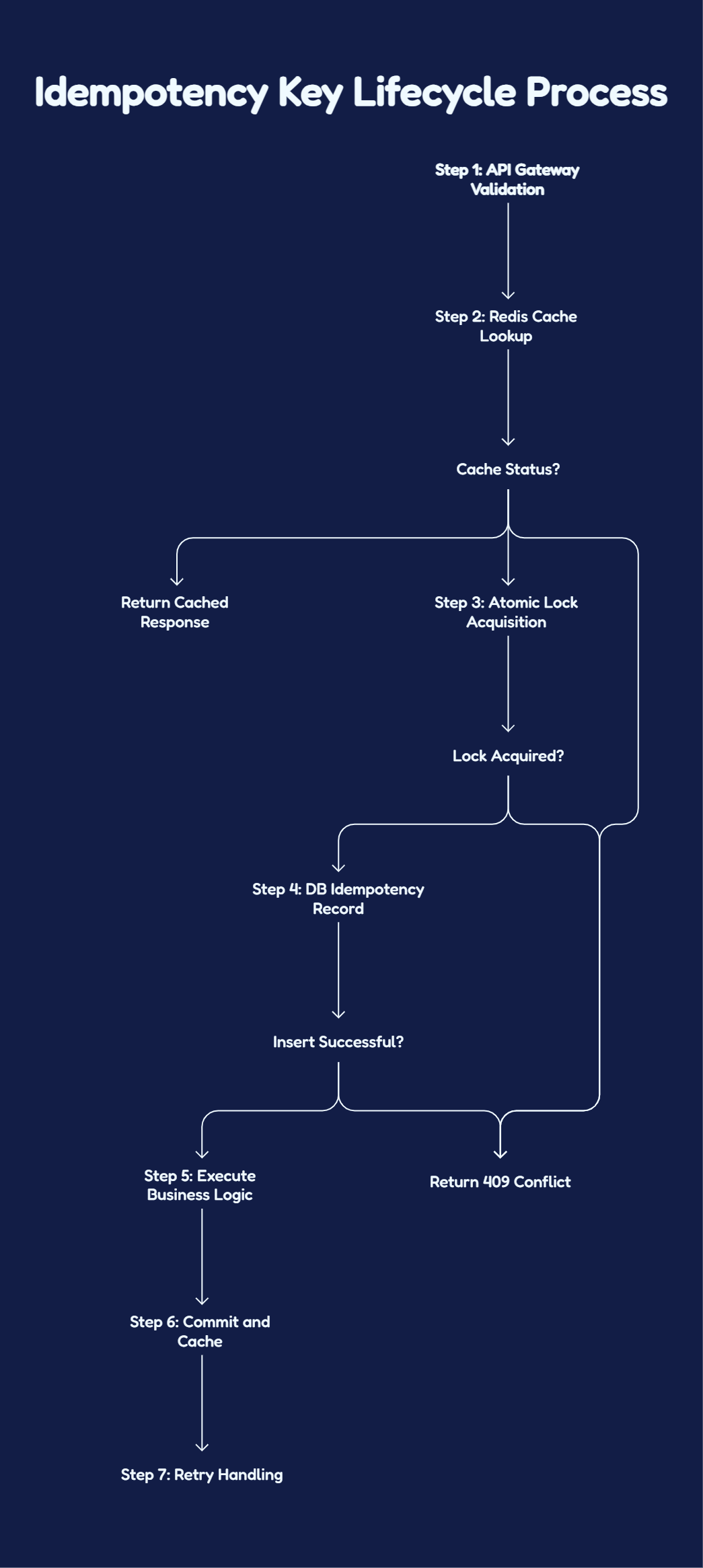

Distributed Idempotency Keys

Every state-mutating payment API endpoint must enforce idempotency by binding each client-generated idempotency_key to a durable response cache — checked before any business logic executes — so that a retried request with an identical key returns the original response without re-executing the payment operation.

| Transaction Type | Duplicate Execution Consequence | Recovery Path |

|---|---|---|

| Card authorization | Double auth hold reduces available credit; second auth may decline due to insufficient funds | Manual void of duplicate auth; requires processor API call; time-bounded (auth hold expiry) |

| RTP / FedNow credit | Second pacs.008 dispatched with new InstrId — two payments settled irrevocably | No network recall; requires recipient cooperation for voluntary return; often unrecoverable |

| ACH origination | Duplicate NACHA file entry creates two entries in next clearing cycle | Return filing (R06/R07) within return window; 2-banking-day recovery; consumer harm in interim |

| Ledger debit | Double debit against customer account; balance driven negative | Manual ledger correction entry; audit trail complexity; Regulation E disclosure obligations |

Idempotency Key Lifecycle

| Cluster Article Candidate

The full implementation specification — Redlock for multi-node Redis HA, TTL sizing for different payment rail latencies, key namespace design for multi-tenant platforms, and load testing idempotency enforcement under retry storms — is covered in: Deep Dive: Implementing Redis-Backed Idempotency for Payment APIs. |

The Transactional Outbox Pattern

Publishing domain events to a message broker must be coupled to the database transaction that produces the state change via a transactional outbox table, because a direct broker publish after a database commit introduces a failure window where the commit succeeds and the publish fails, leaving downstream systems permanently out of sync with ledger state.

| Relay Approach | Mechanism | Latency | Operational Complexity |

|---|---|---|---|

| Polling relay | Dedicated service queries outbox_events WHERE status=’PENDING’ on interval | 100ms–1s | Low — standard application service; no additional infrastructure |

| CDC relay (Debezium) | Kafka Connect + Debezium reads PostgreSQL WAL; outbox table changes stream directly to Kafka | < 50ms | Higher — requires Kafka Connect cluster, Debezium connector management, WAL retention configuration |

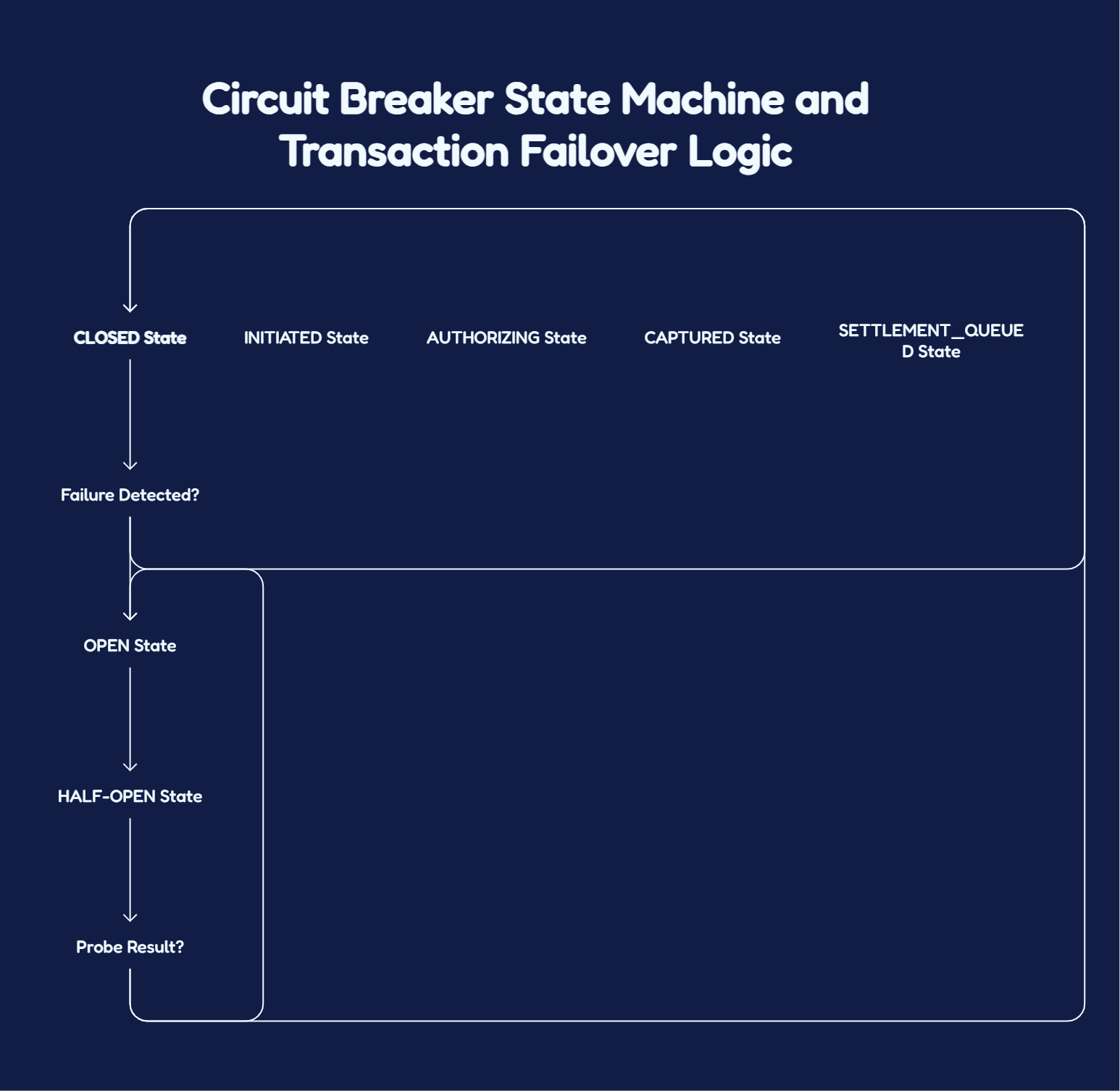

Processor Fallbacks and Circuit Breakers

Payment processor dependencies are external systems with availability SLAs structurally lower than your platform’s 99.999% target. A circuit breaker pattern with active health monitoring and pre-configured fallback routing prevents a single processor outage from translating into platform-wide payment unavailability.

| Transaction State at Circuit Open | Safe to Reroute? | Correct Action |

|---|---|---|

| INITIATED (no processor call yet) | YES | Route to secondary processor using same idempotency_key — secondary has no record of it |

| AUTHORIZING (auth dispatched, no response) | NO | Query primary processor status API first. If unavailable, hold in AUTHORIZATION_PENDING. Do NOT double-authorize on secondary. |

| CAPTURED (auth confirmed, capture in flight) | NO | Do NOT retry capture on secondary — this is a money movement instruction. Hold in CAPTURE_PENDING; reconcile via processor webhook. |

| SETTLEMENT_QUEUED | N/A | Settlement is processor-internal. Monitor settlement file/webhook for confirmation. |

7. Observability, Auditing, and Compliant Simulation Environments

Observability in regulated payment systems is an adversarial design problem where the instrumentation layer itself becomes an audit surface, a data breach vector, and a regulatory liability if not architecturally hardened from the ground up. The same telemetry pipeline that gives your SRE team transaction visibility will, without deliberate scrubbing and access control design, route raw PANs, OAuth tokens, and customer PII directly into plain-text log aggregators that are categorically out of PCI DSS CDE scope.

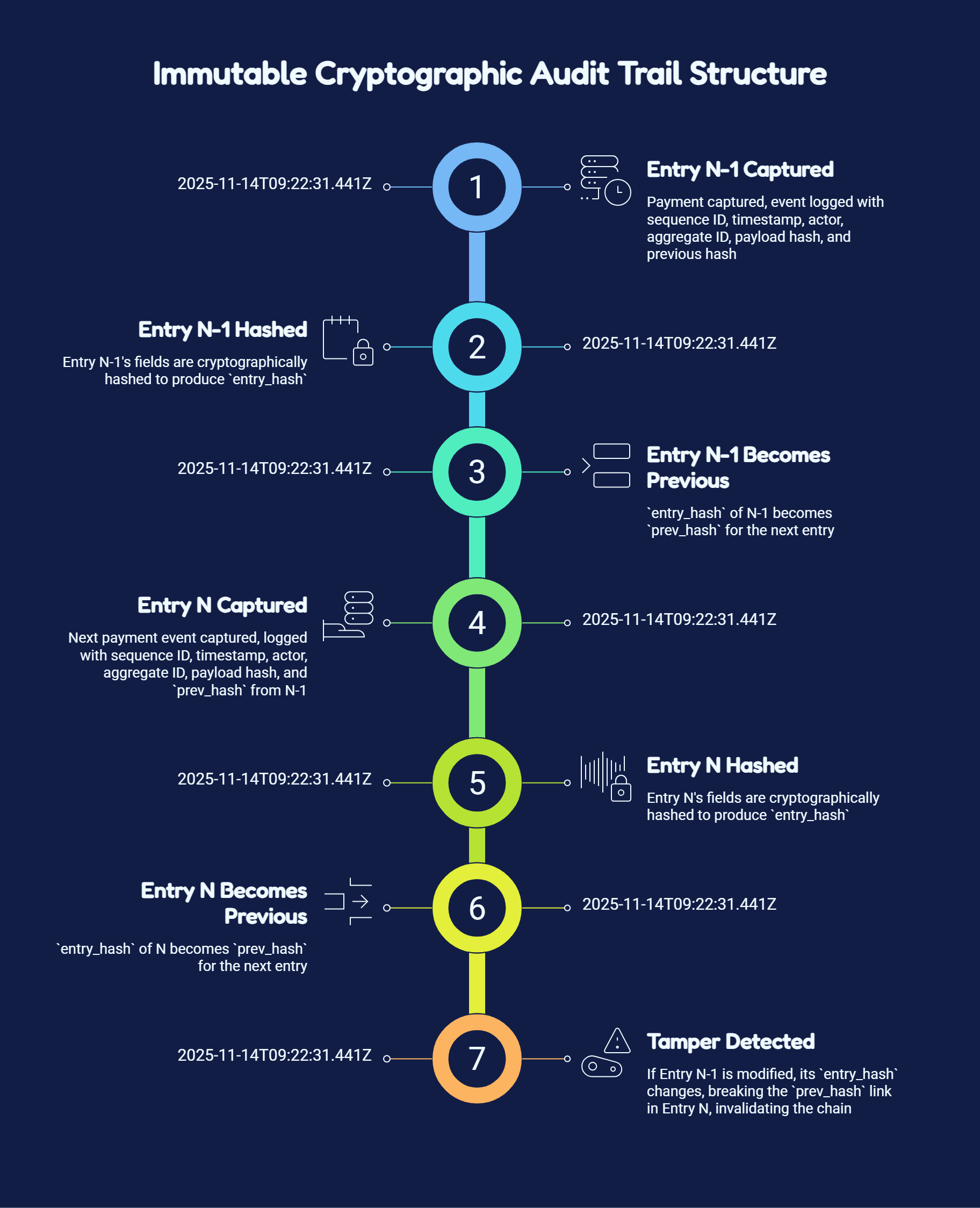

Immutable Cryptographic Audit Trails

A compliant financial audit trail requires append-only log storage where each entry is cryptographically bound to its predecessor via chained hashing — producing a tamper-evident log structure where any retroactive modification of a historical record invalidates all subsequent entries, making falsification detectable without requiring trust in the log storage infrastructure itself.

TAMPER DETECTION:

Modify ANY field in Entry N-1

→ entry_hash(N-1) changes

→ prev_hash(N) no longer matches

→ chain breaks; all subsequent entries invalidated

Auditor re-computes chain from genesis entry:

→ first hash mismatch identifies the tampered record

Zero-Leak Log Scrubbing

Every log emission point in the payment service stack — structured application logs, HTTP access logs, distributed trace spans, APM transaction metadata — must pass through a scrubbing pipeline that detects and redacts PAN patterns, CVV fields, authorization headers, OAuth tokens, and customer PII before the payload reaches any log aggregator.

| ⚠ SECURITY WARNING

A single plain-text PAN in any log line — regardless of the log aggregator, the access control policy on that aggregator, or the intent of the engineer who wrote the log statement — constitutes a PCI DSS Requirement 3.3 violation and a potential reportable data breach under card brand rules. A PAN discovered in a Datadog log index, a Splunk search result, or an Elasticsearch shard places the entire observability infrastructure — every server in the SIEM cluster, every engineer with query access, every data retention policy governing that index — into PCI DSS CDE scope retroactively. Retroactive CDE scope expansion triggers a full re-scoping of the PCI assessment, invalidates the current SAQ-D or ROC, and requires a gap remediation program before re-certification — typically a 3–6 month delay. |

| Scrubbing Rule | Detection Method | Replacement | Why It Matters |

|---|---|---|---|

| PAN detection | Regex pattern + Luhn algorithm validation on candidate strings | [PAN_REDACTED:LAST4=xxxx:BIN=xxxxxx] | Preserves BIN and last-four for debugging; removes middle digits that constitute the PAN |

| CVV detection | Field name matching: cvv, cvc, cvv2, security_code, card_code | [CVV_REDACTED] | CVV must never be persisted (PCI DSS Req. 3.3.1). Field name match catches all formats. |

| Authorization header scrubbing | Regex: Authorization: (Bearer|Basic) \S+ | [TOKEN_REDACTED] | Applies to HTTP request logs and trace span attributes. Prevents OAuth token leakage. |

| PII field pseudonymization | Field allowlist matching against configurable PII field set | HMAC-SHA256(field_value, scrub_key) — truncated 16 chars | Pseudonymization preserves correlation ability for debugging without exposing raw PII. |

| Structured log field allowlist | Pre-approved field name whitelist; unknown fields dropped entirely | Field omitted; counter incremented | Prevents accidental new PII fields from leaking when developers add ad-hoc log context. |

High-Fidelity Mocking and Simulation Frameworks

Payment system test environments that simulate only the happy path will fail to expose the fault-handling gaps that cause production incidents. The failure modes that damage production systems are processor-specific error codes, ISO 20022 formatting edge cases, and network timeout behaviors that must be replicated precisely in a controlled simulation environment.

| Fault Category | Required Simulation Coverage |

|---|---|

| ISO 8583 Processor Decline Codes | 05 Do Not Honor, 14 Invalid Card, 51 Insufficient Funds, 54 Expired Card, 61 Exceeds Withdrawal Limit, 91 Issuer Unavailable, 96 System Malfunction, 1A SCA Required (soft decline) |

| Network & Timeout Behaviors | TCP connection timeout, response after partial send (connection drop mid-payload), HTTP 200 with malformed JSON, duplicate webhook delivery (same event_id 2× within 5s), out-of-order webhooks |

| ISO 20022 Message Faults (RTP/FedNow) | pacs.002 RJCT codes: AC01, AC04, AC06, AG01, AM04, NARR. Schema faults: missing mandatory field, invalid ISO 4217 currency code, amount with decimal, malformed BIC |

| AML / Sanctions Screening Responses | Exact name match (OFAC SDN) → trigger freeze + SAR. Fuzzy match above threshold → manual queue. Vendor timeout → apply fallback rule. Vendor 500 error → block + alert (not pass-through) |

| Cluster Article Candidate

The full specification for high-fidelity payment simulation — including ISO 20022 message generation libraries, BIN range management, chaos scenario catalog design, and contract testing patterns for multi-processor environments — is covered in: A Guide to Building High-Fidelity Banking Simulation Frameworks. |

Regulated Chaos Engineering

Chaos engineering in a regulated payment environment cannot follow the standard ‘inject failure into production and observe’ model. Fault injection must execute in a compliance-equivalent sandbox environment that mirrors production network topology, data classification boundaries, and service dependency graphs, because injecting failures into production systems that touch CDE components requires advance change management documentation and QSA notification under PCI DSS Requirement 6.5.

| Chaos Experiment | Injection Method | Key Success Criteria | Rollback |

|---|---|---|---|

| Database Shard Isolation | iptables DROP on IN shard subnet egress | EU transactions unaffected; IN transactions return HTTP 503 within 2s (not 30s timeout); circuit breaker OPEN within 30s; no ledger entries written for IN transactions | Remove iptables rule; verify shard reconnection |

| Risk Scoring Node CPU Saturation | stress-ng –cpu 8 –timeout 120 on scoring nodes | Primary transaction p99 < 500ms; fallback rule engine activates within 50ms; no transactions approved without any fraud check; scoring degradation alert fires within 60s | Terminate stress-ng; verify CPU normalization |

| Outbox Relay Process Kill | SIGKILL on relay process after 50% of batch published | Restarted relay re-processes PENDING rows only; SKIP LOCKED prevents double processing; Kafka consumer event_id deduplication catches any duplicates; outbox lag clears within 2× normal cycle | Verify relay stable; inspect outbox_events for anomalies |

| mTLS Certificate Expiry | Rotate service certificate to expired test cert via cert-manager annotation override | Affected service returns TLS handshake failure; no fallback to HTTP (verified by packet capture); certificate expiry alert fires; recovery < 5 minutes after cert rotation | Restore valid certificate; verify mTLS handshake |

8. Conclusion: Compliance as a Competitive Engineering Advantage

The payment engineering teams that ship fastest are not the ones that move compliance review to the end of the sprint — they are the ones that made compliance structurally irrelevant to the product sprint in the first place. That is the operational consequence of isolation through abstraction: when the compliance boundary is a first-class structural component, the product layer above it inherits its guarantees without inheriting its constraints.

The Compounding Cost of the Alternative

| Phase | Decision Made | Commercial Consequence |

|---|---|---|

| Phase 1 — Early Stage (Months 0–12) | Defer CDE isolation; skip idempotency framework; co-locate PII and transaction data in monolithic schema | Perceived benefit: faster initial feature velocity. Actual state: compliance debt accumulating silently. |

| Phase 2 — Growth Stage (Months 12–24) | First QSA engagement: full infrastructure in scope. PAN discovered in application logs. Idempotency gaps surface as chargeback rate climbs. | Cost to remediate: 2–4× the original build cost. Timeline: 6–18 months of architectural rework. Feature freeze on all in-scope systems during remediation. |

| Phase 3 — Scale Stage (Months 24–36) | Annual PCI audit cost elevated. Each new market entry requires new compliance assessment. Each new feature requires legal review if it touches any co-located data store. | Compliance is now a literal product bottleneck — every roadmap item requires compliance sign-off that the architecture was supposed to make unnecessary. The debt is always collected. |

Compliance as Velocity: The Architecture That Pays Forward

| Architectural Property | Product Velocity Consequence |

|---|---|

| CDE boundary enforced at network layer | Checkout UI, merchant dashboard, loyalty features, A/B tests — none of these trigger PCI review. Ship without compliance gate. |

| Tokenization abstracts PAN from product layer | New payment methods (BNPL, wallets, account-to-account) integrate against token API — not against CDE internals. No scope expansion. |

| Geo-sharded regional data planes | Entering a new market (UAE, Brazil, Indonesia) requires provisioning a new regional shard — not re-architecting the global data model or obtaining new data transfer mechanisms. |

| Idempotency enforced at framework level | Client SDK, mobile app, and third-party integrations can retry aggressively — the platform absorbs retries safely. Reduces support escalations. |

| Compliance tier decoupled from transaction path | AML rule engine updates, KYC vendor swaps, sanctions list refresh — none block payment processing. Deploy independently. |

| Immutable audit log with chained hashes | QSA audit evidence is generated continuously by the system itself. Audit preparation is a reporting query, not a manual evidence collection project. |