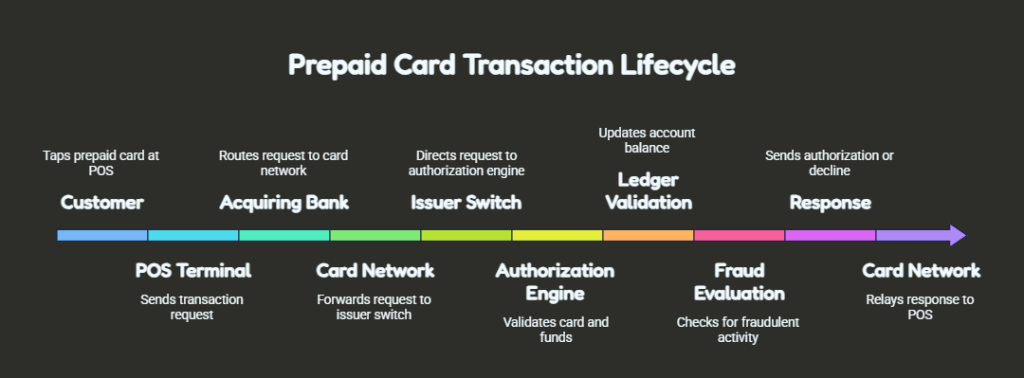

That apparent simplicity masks a carefully orchestrated sequence of API calls, ledger updates, fraud validations, network routing decisions, and settlement workflows involving issuers, acquirers, payment networks, and backend financial systems.

As embedded finance reshapes industries, non-fintech businesses — retailers, logistics providers, healthcare organizations, travel companies, enterprise platforms — are integrating open-loop card capabilities directly into their products.

Rather than becoming banks themselves, they rely on a card issuance platform that handles regulatory complexity while exposing programmable APIs for card lifecycle management and transaction processing.

This article follows a transaction from tap to authorization, ledger recording, clearing, and settlement — and along the way, walks through what it actually takes to plug into one of these platforms.

What Is an Open-Loop Card?

Open-loop cards run on globally accepted payment networks — Visa, Mastercard, RuPay, and regional schemes. Unlike closed-loop cards, which only work within a single merchant’s ecosystem, open-loop cards work anywhere the underlying network is accepted.

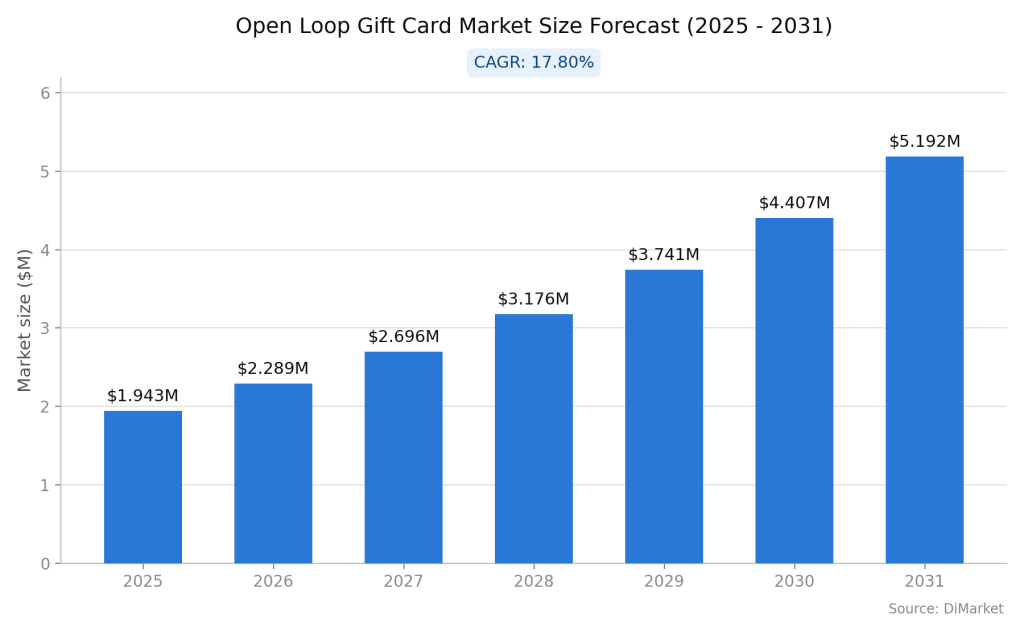

The scale of this shift isn’t theoretical. Market research firm DiMarket projects the open-loop gift card market growing from roughly $1.943M in 2025 to $5.192M by 2031 — a 17.80% CAGR. That kind of sustained growth is exactly why the underlying issuance and ledger architecture matters: platforms built on shortcuts today are the ones that end up re-architected under load a few years in.

Payroll cards, corporate expense cards, travel and forex cards, general-purpose prepaid cards, government benefit cards, and network-backed gift cards all fall into this category.

Payroll cards are a good illustration of the stakes involved: C3Pay, a WPS-compliant payroll card program built for Edenred UAE, processes salaries for millions of workers on exactly this open-loop rail. Because each of these touches multiple financial institutions, payment networks, and regulatory regimes at once, the supporting technology stack is considerably more complex than a typical wallet application.

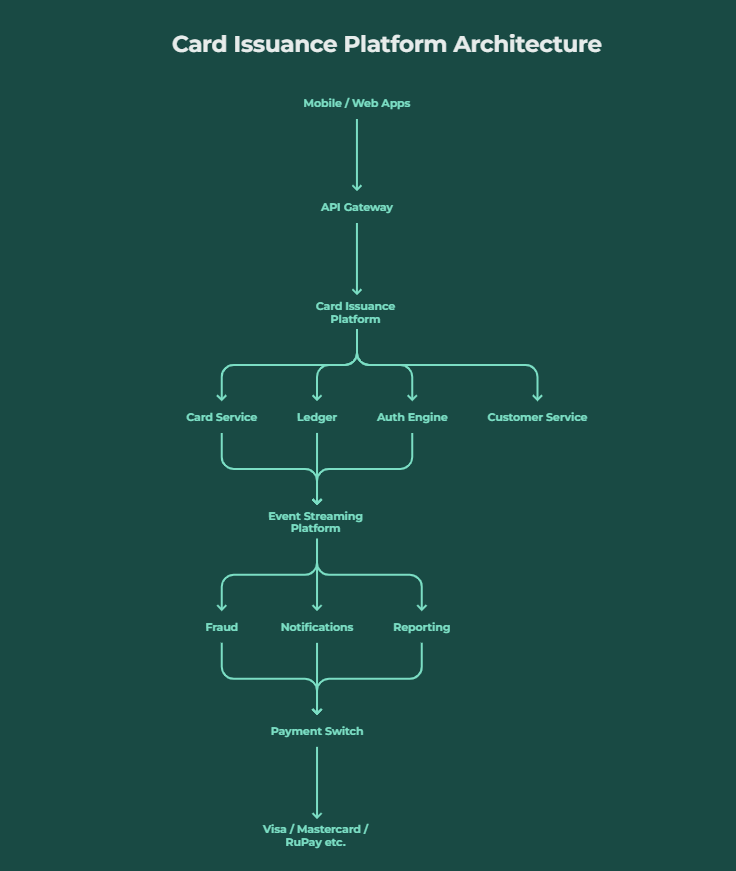

The Role of a Card Issuance Platform

Getting from sandbox to production

Core Components of a Modern Card Issuance Platform

Each service owns one business capability and communicates with the others asynchronously through events wherever possible — a design choice that matters a lot once you get to the failure-handling discussion below.

Understanding the Transaction Lifecycle

Ahamed Sajid is a technology delivery leader focused on building scalable systems that bridge business strategy and execution. With experience across fintech, mobility, e-commerce and enterprise platforms, he specializes in designing structured approaches to complex problem-solving and product delivery. He is particularly interested in how well-defined systems, processes, and technology frameworks can drive sustainable growth and operational clarity. Through his work, Ahamed advocates for pragmatic innovation where ideas are shaped into reliable, high-impact solutions that deliver real-world value.