How non-fintech companies can leverage Banking-as-a-Service, white-label wallets, and fintech API integration to unlock new revenue streams

Introduction: Finance Is Eating the World

A decade ago, if you wanted to offer your customers a digital wallet, a loan, or an international money transfer, you needed a banking licence, a compliance team, and a multi-year technology build. Today, you need none of those things.

This is the essence of embedded finance — and it is quietly reshaping every industry on the planet. From ride-hailing apps that pay drivers instantly to e-commerce platforms offering buy-now-pay-later at checkout, the line between financial services and everyday software has all but disappeared.

The numbers tell the story. The global embedded finance market is projected to exceed USD 7 trillion in transaction value by 2030. Yet most businesses — retailers, logistics companies, healthcare platforms, government portals — are still treating payments as an afterthought rather than a strategic asset.

This blog breaks down how embedded finance actually works, what it takes to build it right, and how companies in virtually any industry can use it to deepen customer relationships, unlock new revenue streams, and future-proof their business.

1. What Is Embedded Finance — And Why Does It Matter Now?

Embedded finance is the seamless integration of financial products and services directly into non-financial platforms and applications. Rather than redirecting users to a bank, the financial service lives natively inside the product experience they are already using.

Think of it this way: when a user books a cab and the app automatically splits the fare, applies a loyalty cashback, and settles the driver in real-time — that is embedded finance at work. The user never leaves the app. The business never needs a banking licence. The technology does the heavy lifting.

Why is embedded finance accelerating now?

- Open banking regulations in Europe, India (via UPI), the Middle East, and the US have forced financial infrastructure to become programmable.

- Banking as a Service (BaaS) providers now offer modular, API-first infrastructure that can be licensed and white-labelled in weeks rather than years.

- Consumer expectations have shifted — people expect financial convenience inside every app, not a separate banking app.

- Fintech API integration costs have plummeted, making the economics work for mid-sized and even small businesses.

The result is a world where a logistics company can become a payments company, a retailer can become a lender, and a government portal can become a digital bank — all without changing their core business.

2. The Architecture of Embedded Finance: BaaS, APIs, and White-Label

Understanding how embedded finance works requires understanding its three foundational layers.

Layer 1: Banking as a Service (BaaS)

Banking as a Service (BaaS) is the backbone of embedded finance. A BaaS provider holds the regulatory licences, maintains the core banking infrastructure, and exposes it all via APIs. Businesses consume these services without needing their own banking charter. BaaS covers account issuance, KYC and AML compliance, card issuance, payment processing, and regulatory reporting. The business builds the customer experience; the BaaS provider handles everything underneath.

Layer 2: Fintech API Integration

APIs are the connective tissue. Fintech API integration allows businesses to plug specific financial capabilities — payments, wallets, lending, foreign exchange, insurance — directly into their existing applications. A single API call can trigger a cross-border remittance to 150 countries, issue a virtual card, or disburse a micro-loan. Mindster builds and integrates these API layers, working with payment networks, money transfer operators, card schemes, and local payment systems to create unified middleware that speaks the language of each underlying system while presenting a clean, consistent interface to the business.

Layer 3: White-Label Financial Services

White-label financial services allow a business to offer a fully branded financial product — digital wallet, remittance app, loyalty system — built on proven underlying technology. The customer sees your brand; the technology behind the scenes is ours. This approach dramatically reduces time-to-market, lowers regulatory risk, and allows businesses to focus on customer acquisition and experience rather than infrastructure.

3. Deep Dive: Mindster’s Digital Wallet Module

Our Digital Wallet module is the most deployed component of our embedded finance stack. It powers peer-to-peer transfers, bill payments, loyalty rewards, top-ups, and multi-currency holdings across a single, configurable platform.

What the wallet does

- Peer-to-peer money transfer between registered users — instantly, with full audit trail

- Bill payments across multiple service categories (utilities, telecom, insurance, government fees)

- Closed-loop and semi-closed-loop wallet configurations to meet regulatory requirements in different jurisdictions

- Loyalty engine integration — every transaction can earn and burn points, cashback, or vouchers

- Virtual and physical card issuance linked to wallet balances

- Multi-currency wallets for businesses operating across borders

- Real-time transaction notifications and spending analytics

The middleware advantage

One of the most underestimated challenges in wallet deployment is integration complexity. A wallet needs to connect to the core banking system, the payment switch, the card network, the loyalty engine, government payment gateways, and the mobile app — simultaneously.

Mindster builds a bespoke middleware layer that acts as the integration orchestrator. This was precisely the architecture we deployed for ONEIC Pay, where our middleware connected a peer-to-peer wallet, 12 bill payment services, a loyalty system, and multiple backend systems into a single coherent mobile experience. The result: 1 million+ users and 20,000+ daily transactions, with loyalty features driving a 30% increase in transaction volume within six months.

ONEIC Pay — Results at a Glance

| Metric | Result |

|---|---|

| Active users | 1 million+ |

| Daily transactions | 20,000+ |

| Bill payment services | ~12 integrated services |

| Transaction growth | +30% in 6 months (loyalty) |

| Architecture | Peer-to-peer wallet + middleware + loyalty engine |

4. Deep Dive: The Money Exchange & International Remittance Module

Cross-border remittance is one of the largest and most underserved markets in financial services. Globally, over USD 800 billion is remitted annually, yet millions of migrant workers and small businesses still pay high fees and experience multi-day settlement windows. Our Money Exchange module changes that.

Core capabilities

- International remittance to 150+ countries through Western Union and other operator integrations

- Real-time foreign exchange rate display with live rate feeds

- Multi-corridor support — optimised routing for cost and speed by destination country

- WPS (Wage Protection System) compliance for GCC markets, ensuring salary disbursements meet regulatory requirements

- BENEFITPay and local payment network integrations for Bahrain, UAE, Oman, and other GCC jurisdictions

- Beneficiary management — users can save, verify, and reuse recipient bank details

- KYC and AML screening at the point of transaction initiation

- Full transaction audit trail for regulatory reporting

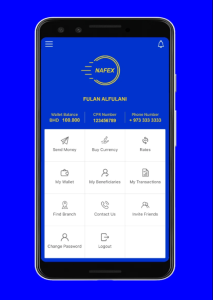

NAFEX — White-Label Remittance at Scale

National Finance Exchange (NAFEX) in Bahrain is a textbook example of how a traditional money exchange company can be transformed into a fully digital remittance platform using our white-label stack. We delivered a complete mobile app and middleware platform that connected NAFEX’s backend systems to Western Union’s global transfer network (covering 150+ countries), integrated BENEFITPay for local Bahraini payments, and embedded WPS compliance directly into the salary disbursement workflow. The result: 100,000+ app downloads and a business that can now compete with the largest digital remittance players in the region — all under their own brand.

How non-fintech companies can use this

Here is the important insight: NAFEX is a money exchange company. But the same platform can be deployed by a logistics company paying drivers in 30 countries, a staffing agency disbursing wages to workers across the GCC, an e-commerce marketplace settling international supplier payments, or a government agency distributing welfare benefits to citizens abroad.

The white-label architecture means the technology is the same. The brand, the UX, the onboarding flow, and the compliance configuration are tailored to each client. Time to market: 12–20 weeks depending on integration complexity.

5. How Non-Fintech Companies Can Embed Financial Services

The most exciting opportunity in embedded finance is not for fintech startups. It is for established non-financial businesses that already have large, engaged customer bases and deep domain knowledge in their industry. Adding financial services to these businesses creates a flywheel: more utility drives more engagement, which drives more data, which enables better financial products, which drives more utility.

Retail & E-Commerce

An e-commerce platform that processes millions of orders already has rich spending data. Embedding a closed-loop wallet with loyalty rewards increases basket size and reduces payment friction. Adding embedded lending solutions (buy-now-pay-later, micro-credit) at checkout converts browsers into buyers. Our loyalty engine, deployed for IM Fab Star, distributed INR 2.5 crore in rewards within one year of launch.

Logistics & Gig Economy

A logistics company with 10,000 drivers needs to pay them quickly, accurately, and compliantly. Embedding a digital wallet into the driver app — funded by the company, accessible instantly after delivery completion — eliminates bank transfer delays and dramatically improves driver satisfaction and retention.

Government & Public Sector

Government portals that consolidate citizen services are a natural home for embedded payments. GoNPay is our deployment for a unified government payment platform that allows citizens to pay utility bills, fines, and municipal services in one place — earning loyalty points on every transaction. KVVES, a Kerala-based welfare organisation, used our platform to digitise INR 100 crore+ in welfare fund collections and disbursements.

Healthcare & Insurance

Healthcare platforms can embed insurance premium collection, claim disbursement, and medical credit directly into the patient journey. Embedded lending solutions tied to health spending can increase access to treatment while creating a new revenue line for the platform.

Manufacturing & B2B

B2B businesses face unique embedded finance opportunities: supply chain financing, early payment discounts, multi-tier loyalty for distributors and dealers. Our IM Fab Star deployment for India’s IM Steel group shows how a manufacturing company can use a loyalty wallet to incentivise and track dealer performance across a complex distribution network.

Also explore How to Design a Fintech Application: A Step-by-Step Approach

6. The Mindster Embedded Finance Playbook

Over 20+ years of product engineering, we have developed a repeatable approach to embedded finance deployment that minimises risk and accelerates time to value.

Step 1: Define the Financial Use Case Not every business needs every financial product. We start by identifying the single highest-value financial service for your customer base — typically: reduce payment friction (wallet/embedded payments in apps), reward loyalty (loyalty + wallet), or expand access (embedded lending solutions or remittance).

Step 2: Choose the Right Architecture Depending on your regulatory environment and integration complexity, we design the right stack: a fully white-label solution built on our existing modules, a BaaS integration connecting to a licenced third-party banking infrastructure, or a custom middleware layer connecting your existing systems to financial APIs.

Step 3: Compliance-First Build Every market has its own regulatory requirements. Our team has deployed compliant solutions in India (RBI, UPI), GCC (WPS, SAMA, CBB, CBUAE), and Africa. We build compliance into the architecture from day one — KYC/AML workflows, transaction monitoring, regulatory reporting, and data residency requirements.

Step 4: Launch MVP, Then Scale Our agile methodology launches a focused MVP in 12–20 weeks. We then iterate based on user data, adding features and expanding to new corridors or product categories as the business grows.

Mindster Fintech by the Numbers

| 3M+ Users | 125M+ Transactions | $20B+ Transaction Value | 4.2★ Avg Rating |

|---|

Conclusion: Your Business Can Be a Fintech

The barriers that once reserved financial services for banks and licenced institutions have fallen. Embedded finance integration is no longer a competitive advantage for fintech startups — it is a competitive necessity for every business that processes transactions, manages a workforce, or serves customers at scale.

Whether you want to launch a white-label digital wallet for your customers, embed international remittance into your platform, build a loyalty-driven payments ecosystem, or offer embedded lending solutions to your user base — the technology, the expertise, and the track record exist today.

At Mindster, we have built this infrastructure for banks, airlines, government agencies, retailers, and startups across three continents. We know what works, what breaks, and how to move fast without breaking things.

Ready to turn your business into a fintech? Let’s talk.

Professional content writer Akhila Mathai has over four years of experience. She writes posts about the different mobile app solutions we offer as well as services related to them. Her ability to conduct thorough research and think critically enables her to produce excellent, authentic, and legitimate content. Along with her strong communication abilities, she collaborates well with her teammates to create information that is current and relevant to emerging technology.